Most people focus on how much they earn.

Far fewer pay attention to how much they silently lose.

And that difference – the gap between what you earn and what you actually keep – often comes down to a three-digit number most people check once and forget.

Your credit score.

It doesn’t feel urgent. It doesn’t announce itself. But every time you borrow money – for a home, a car, a credit card – it shapes the terms. Quietly. Permanently. At a cost most people never calculate.

This post does the math.

THE MECHANISM: HOW LENDERS USE YOUR SCORE TO SET YOUR RATE

When you apply for a loan, a lender faces one central question: how likely is this person to pay us back?

They can’t know your intentions. They can’t assess your character. What they can do is look at your track record – and your credit score is the compressed version of that track record, distilled into a number from 300 to 850.

A higher score signals lower risk. Lower risk means the lender is more confident they’ll be repaid – so they can afford to charge less for the use of their money.

A lower score signals higher risk. Higher risk gets offset with a higher interest rate – effectively charging you for the statistical probability that you may not pay as reliably as a higher-scoring borrower.

The result: two people borrowing the same amount, for the same purpose, on the same day, can pay dramatically different amounts of money – simply because their credit histories diverged.

“A higher interest rate isn’t a punishment. It’s a price. The price lenders charge for uncertainty. And your credit score is what determines that price.”

THE REAL NUMBERS: WHAT YOUR SCORE ACTUALLY COSTS YOU

This is where most articles stay vague. This one won’t.

The figures below are approximate and illustrative – actual rates vary by lender, loan type, and market conditions. But the relationships between credit score tiers and interest rates are consistent and well-documented.

Mortgages: Where the Gap Is Largest

On a 30-year fixed mortgage, the difference between a strong credit score and a weak one translates into one of the most significant financial gaps in personal finance.

| Credit Score | Approx. Rate | Monthly Payment ($300K) | Total Interest Paid |

|---|---|---|---|

| 760 – 850 | ~6.5% | ~$1,896 | ~$382,000 |

| 700 – 759 | ~6.75% | ~$1,946 | ~$400,500 |

| 680 – 699 | ~7.0% | ~$1,996 | ~$419,000 |

| 660 – 679 | ~7.25% | ~$2,047 | ~$437,000 |

| 640 – 659 | ~7.75% | ~$2,152 | ~$475,000 |

| 620 – 639 | ~8.25% | ~$2,254 | ~$511,500 |

Figures are illustrative. Rates vary by lender, market conditions, and loan type. Always get multiple quotes.

The gap between a 760 score and a 620 score on a $300,000 mortgage: roughly $358 per month and $129,000 in total interest over the life of the loan.

That’s not a rounding error. That’s a retirement account’s worth of money – redirected to a lender instead of your future.

Auto Loans: Where the Impact Hits Fastest

Auto loans tend to carry higher rates than mortgages, and the credit score spread is even more pronounced.

| Credit Score | Approx. Rate | Monthly Payment ($30K / 60 mo.) | Total Interest |

|---|---|---|---|

| 750+ | ~6% | ~$580 | ~$4,800 |

| 700 – 749 | ~8% | ~$608 | ~$6,500 |

| 650 – 699 | ~12% | ~$667 | ~$10,000 |

| 620 – 649 | ~16% | ~$731 | ~$13,900 |

| Below 620 | ~20%+ | ~$797+ | ~$17,800+ |

Figures are illustrative. Rates vary significantly by lender, term, and vehicle type.

A borrower with a 620 score pays roughly $151 more per month than a borrower with a 750 score on the same car – and over $9,000 more in total interest.

Every month. For five years. For the exact same vehicle.

Credit Cards: The Silent Compounding Trap

Credit card APRs are where a weak credit score can inflict the most sustained damage – because balances that aren’t paid in full carry interest charges that compound monthly.

| Credit Score | Typical APR Range |

|---|---|

| 750+ (Excellent) | 18% – 21% |

| 700 – 749 (Good) | 22% – 24% |

| 650 – 699 (Fair) | 26% – 28% |

| Below 650 (Poor) | 29% – 35%+ |

Rates vary by issuer and card type.

At a 35% APR, a $5,000 balance carried for two years costs roughly $1,900 in interest – more than twice what the same balance would cost someone carrying the premium-tier rate.

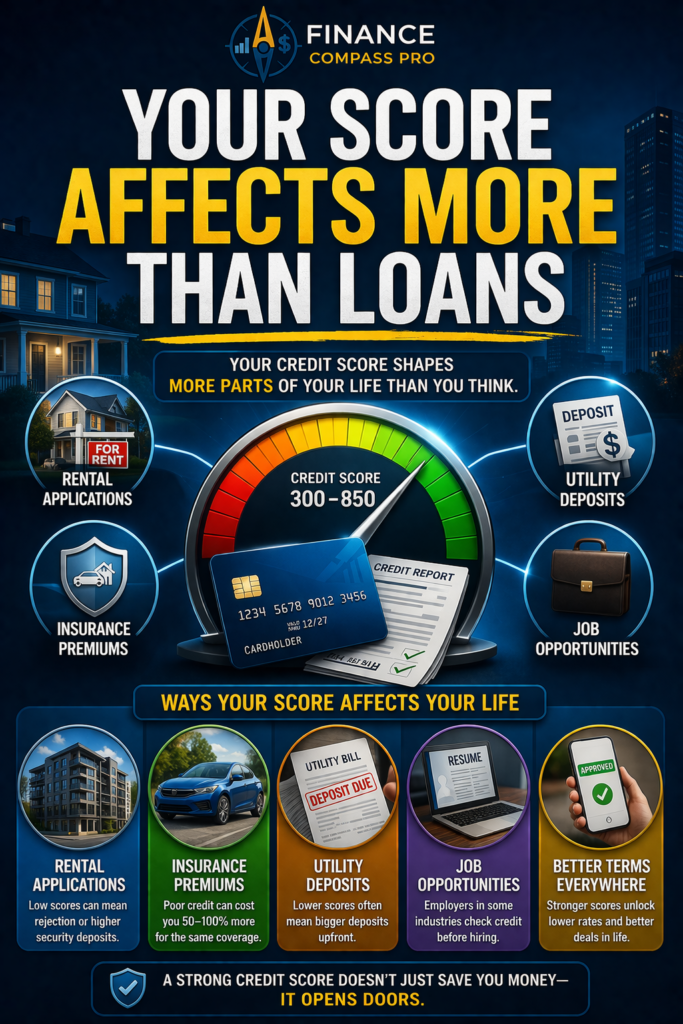

IT’S NOT JUST BORROWING: THE WIDER REACH OF YOUR SCORE

Most people know their credit score affects loans. Fewer realize how far that influence extends.

Rental applications. Most landlords in major metro areas pull credit as part of screening. A score below 650 can result in rejection or a requirement for a larger security deposit – often one to two months’ additional rent upfront.

Insurance premiums. In most U.S. states, insurers use credit-based insurance scores to set auto and home insurance rates. Drivers with poor credit can pay 50-100% more for identical coverage compared to drivers with excellent credit.

Utility deposits. Providers often require a security deposit from customers with low credit scores – typically $150-$300 – before activating service. Customers above the threshold pay nothing upfront.

Employment screening. Certain roles – particularly in finance, security, or positions handling sensitive information – include a credit check as part of background screening.

The same score that sets your mortgage rate is quietly influencing costs across multiple areas of your life simultaneously.

“Your credit score doesn’t just determine what you pay when you borrow. It shapes the cost of living in ways most people never connect to a three-digit number.”

THE COMPOUNDING LOGIC: WHY THIS MATTERS MORE THAN YOU THINK

Here’s the arithmetic that makes this urgent.

Take the mortgage example. A borrower with a 620 score pays $358 more per month than one with a 760 score on the same loan.

That’s $4,296 per year.

If that $4,296 had been invested instead – at a modest 7% average annual return – it would compound into roughly $430,000 over 30 years.

The cost of a weak credit score isn’t just the extra interest paid. It’s the wealth that extra interest could have built if the structure had been more efficient from the start.

This is why addressing your credit score is not a cosmetic financial improvement. It’s a structural one. Fix the score, and every financial decision that follows operates on better terms.

WHAT YOU CAN DO ABOUT IT

The good news: credit scores are not fixed. They’re calculated from inputs that respond to behavior – and that behavior can change.

The highest-impact moves, in order of speed:

1. Reduce your credit utilization below 30%. This is the fastest lever – utilization is recalculated monthly, so paying down balances can show results within one billing cycle.

2. Set up automatic minimum payments on every account. Payment history is 35% of your score. One missed payment can drop your score by 50–100 points. Automate the floor.

3. Dispute errors on your credit report. Incorrect late payments, wrong balances, or fraudulent accounts can suppress your score by 50+ points. Fixing them costs nothing and can produce immediate improvement.

4. Stop applying for new credit unnecessarily. Each hard inquiry has a small negative impact. Multiple applications in a short window compound the effect at exactly the wrong time.

For the full step-by-step plan:

→ How to Improve Your Credit Score Fast in 30 Days

And if you want to understand the full mechanics behind how your score is calculated before you start optimizing it:

→ What Is a Credit Score? Everything Beginners Need to Know

THE BIGGER PICTURE

Lower interest rates don’t just reduce monthly payments.

They free up cash flow that can go toward investing. They reduce total debt load faster. They create financial flexibility that compounds over time into real wealth.

A credit score is leverage – quiet, structural, permanent. The people who understand this don’t just manage their credit. They use it as an active part of their wealth-building strategy.

Once your borrowing costs drop, the next move is to redirect what you’re saving:

→ Investing for Beginners: The Complete Guide to Building Wealth in 2026

This article is for informational and educational purposes only and does not constitute financial advice. Interest rate figures used in this post are approximate and illustrative – actual rates vary by lender, market conditions, loan type, and individual profile. No affiliate relationships are currently in place for any tools or services mentioned. Always consult a qualified financial professional before making financial decisions.

Pingback: How to Improve Your Credit Score Step by StepHow to Improve Your Credit Score Step by Step -

Pingback: Passive Income From ETFs: How to Build Monthly Cash Flow With Minimal EffortPassive Income From ETFs: Build Cash Flow Without Managing Individual Stocks -