You’ve decided to start investing. Smart move.

But then you open a brokerage app and see words like “expense ratio,” “dividend yield,” and “asset allocation” – and suddenly it feels like a foreign language.

You’re not alone. Most people never learned this stuff in school.

Here’s the good news: you don’t need an MBA to understand investing. You just need to know the right 10 terms.

Master these, and the rest of the financial world starts to make a lot more sense.

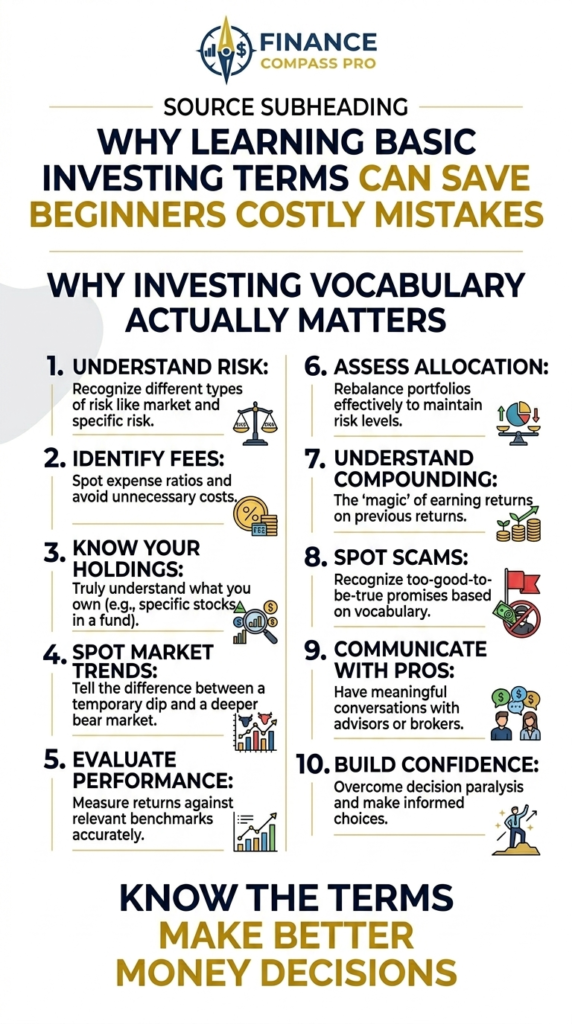

Why Investing Vocabulary Actually Matters

It’s not about sounding smart at dinner parties.

When you understand what these terms mean, you make better decisions. You stop clicking the wrong buttons. You stop panicking when the market drops.

“Financial literacy is not a luxury – it’s a survival skill for your money.”

Let’s break down the 10 most important investing terms, one by one.

The 10 Essential Investing Terms

| # | Term | One-Line Definition |

|---|---|---|

| 1 | Portfolio | Your entire collection of investments |

| 2 | Asset Allocation | How your money is split between investment types |

| 3 | Diversification | Spreading money to reduce risk |

| 4 | Compound Interest | Earning interest on your interest |

| 5 | Expense Ratio | Annual fee charged by a fund |

| 6 | Dividend | Cash payment from a company to shareholders |

| 7 | Index Fund | A fund that tracks a market index |

| 8 | Bull Market / Bear Market | Rising vs. falling market conditions |

| 9 | Risk Tolerance | How much loss you can emotionally handle |

| 10 | Dollar-Cost Averaging | Investing fixed amounts on a schedule |

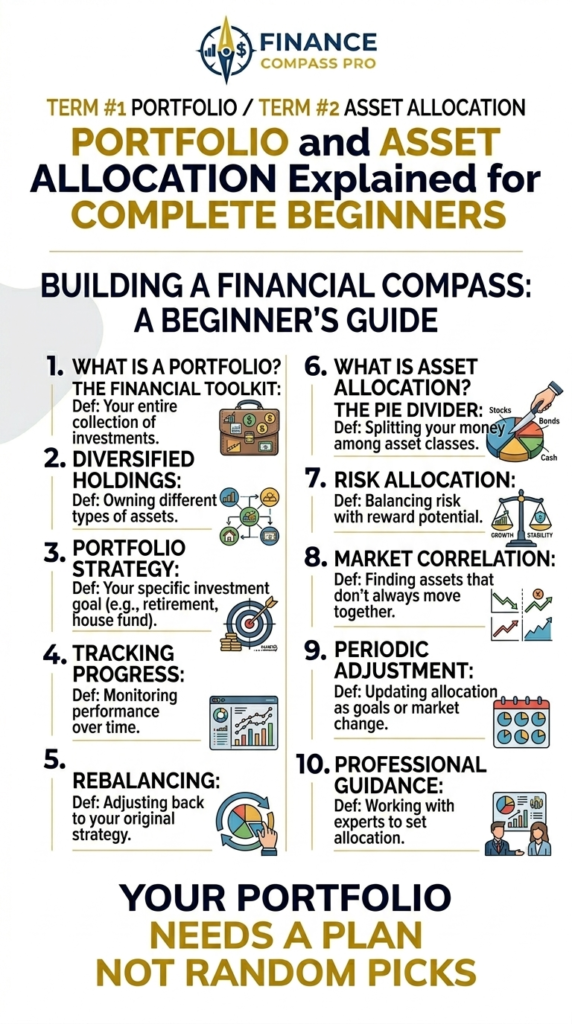

Term #1: Portfolio

A portfolio is the full collection of everything you’ve invested in.

Think of it like a financial closet. Inside might be stocks, bonds, ETFs, real estate, or cash. Together, they make up your portfolio.

You might hear people say things like: “My portfolio is down 5% this month.” They’re not talking about one stock. They mean the whole thing.

Why it matters: Thinking in terms of your whole portfolio – not individual picks – is how serious investors operate. One bad stock hurts less when it’s just 5% of a larger portfolio.

Term #2: Asset Allocation

Asset allocation is how you divide your money across different types of investments.

The most common split is between stocks and bonds. A classic beginner allocation might look like:

- 80% stocks

- 20% bonds

But it depends on your age, goals, and risk tolerance (more on that below).

Why it matters: Asset allocation is one of the biggest drivers of long-term returns. Studies suggest it explains more than 90% of portfolio performance over time.

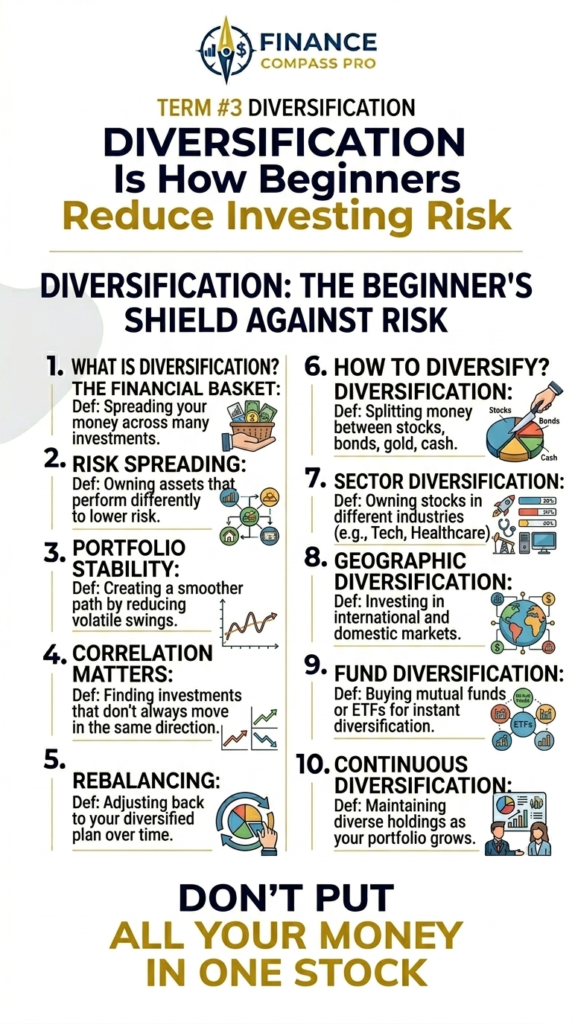

Term #3: Diversification

Diversification means not putting all your eggs in one basket.

Instead of buying one stock, you buy many. If one company fails, your entire savings doesn’t vanish.

“Diversification is the only free lunch in investing.” – Harry Markowitz, Nobel Prize winner

Why it matters: Single stocks can drop 50%, 70%, even 90%. A diversified portfolio of 500 companies? Much more stable. That’s why index funds are so popular with beginners. Learn more in our guide on What Is Diversification in Investing? (The Smart Way to Reduce Risk)

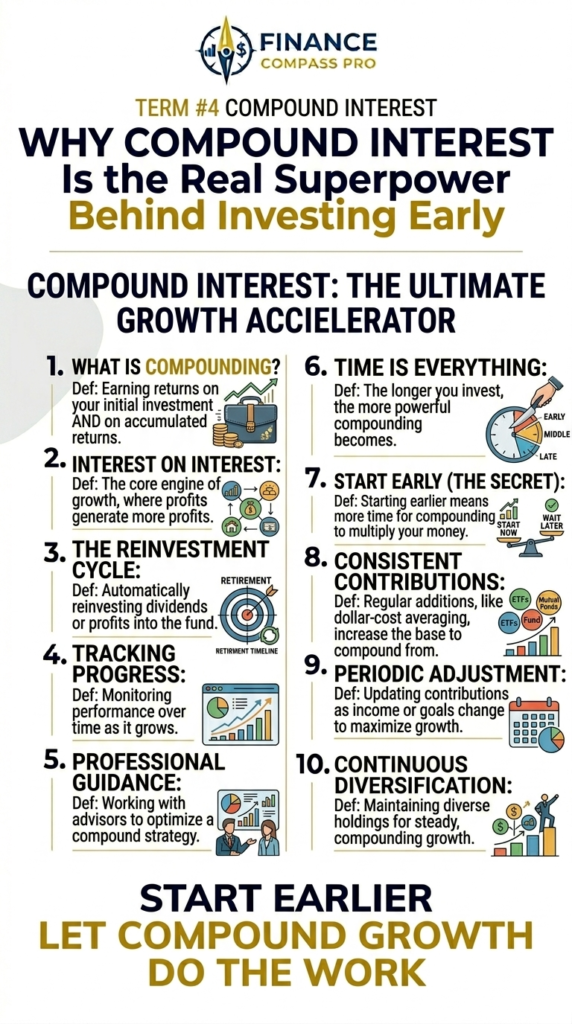

Term #4: Compound Interest

Compound interest is when your money earns returns, and then those returns earn returns too.

A simple example:

- You invest $1,000

- It grows 8% in Year 1 → now $1,080

- It grows 8% in Year 2 on $1,080 → now $1,166

You didn’t add any money. But the interest compounded on itself.

Over 30 years at 8%, that $1,000 becomes over $10,000.

Why it matters: The earlier you start, the more powerful this becomes. Time is your biggest advantage as a young investor.

Term #5: Expense Ratio

An expense ratio is the annual fee a mutual fund or ETF charges you to manage your money.

It’s expressed as a percentage. A 0.03% expense ratio means you pay $3 per year on every $10,000 invested.

| Fund Type | Typical Expense Ratio |

|---|---|

| Index ETF (e.g., VOO) | 0.03% – 0.10% |

| Actively Managed Fund | 0.50% – 1.50% |

| Hedge Fund | 1.50% – 2.00%+ |

Why it matters: Fees compound just like returns – but in reverse. A 1% fee doesn’t sound like much. Over 30 years, it can cost you tens of thousands of dollars.

Term #6: Dividend

A dividend is a cash payment that a company sends to shareholders – usually every quarter.

If you own 100 shares of a company that pays a $0.50 dividend per share, you receive $50 in cash.

Some companies pay generous dividends (utilities, consumer staples). Others pay nothing (growth stocks like Amazon historically).

Why it matters: Dividends can be a form of passive income. Many investors reinvest them automatically to buy more shares, compounding their position over time.

Term #7: Index Fund

An index fund is a type of investment fund that tracks a market index – like the S&P 500.

Instead of a manager picking stocks, the fund just holds all (or most of) the stocks in the index.

The S&P 500 index fund holds 500 of the largest U.S. companies: Apple, Microsoft, Amazon, and so on.

Why it matters: Index funds are low-cost, diversified, and historically outperform most actively managed funds over the long run. They’re the starting point most financial experts recommend for beginners. See our full guide: What Is an Index Fund? A Beginner’s Guide to Smart Investing

Term #8: Bull Market vs. Bear Market

A bull market is when stock prices are rising – generally up 20% or more from a recent low.

A bear market is the opposite – prices fall 20% or more from a recent high.

Bull = charging up. Bear = swiping down. That’s how traders remember it.

Historical context:

- The average bull market lasts about 5.5 years

- The average bear market lasts about 9.6 months

Why it matters: Knowing the cycle helps you stay calm. Bear markets are temporary. Selling during one locks in your losses permanently.

Term #9: Risk Tolerance

Risk tolerance is how much market volatility and potential loss you can handle – emotionally and financially.

Ask yourself honestly: If your $10,000 portfolio dropped to $6,000 overnight, would you:

a) Stay calm and hold

b) Panic and sell everything

If you answered (b), you have low risk tolerance. That’s not bad – it just means your portfolio should lean more conservative.

Why it matters: Investing beyond your risk tolerance leads to panic selling at the worst time. Know your limits before the market tests them.

Term #10: Dollar-Cost Averaging (DCA)

Dollar-cost averaging means investing a fixed dollar amount at regular intervals – regardless of what the market is doing.

Example: You invest $200 every month into an S&P 500 index fund. When prices are high, you buy fewer shares. When prices dip, you automatically buy more.

Over time, this smooths out your average cost per share.

Why it matters: DCA removes emotion from investing. You stop trying to time the market (which almost never works). You just keep buying. See our deep dive: What Is Dollar-Cost Averaging and Why Smart Investors Use It

Quick-Reference Glossary Table

| Term | Plain-English Meaning | Why Beginners Care |

|---|---|---|

| Portfolio | All your investments combined | The big picture of your wealth |

| Asset Allocation | How money is divided by type | Determines your risk/reward |

| Diversification | Spreading across many investments | Reduces risk of ruin |

| Compound Interest | Returns earning returns | The magic of long-term investing |

| Expense Ratio | Annual fund management fee | Hidden cost that compounds against you |

| Dividend | Cash payout from company profits | Passive income from stocks |

| Index Fund | Fund that tracks a market index | Low-cost, beginner-friendly |

| Bull/Bear Market | Rising/falling market cycles | Context for staying calm |

| Risk Tolerance | Your comfort level with loss | Determines right portfolio mix |

| Dollar-Cost Averaging | Investing fixed amounts on schedule | Removes emotion from investing |

What to Learn Next

These 10 terms are your foundation. With them, you can read most financial articles and understand what your brokerage account is actually doing.

Ready to go deeper? Start here:

- Investing for Beginners: The Complete Guide

- How to Start Investing With $100: A Beginner’s Step-by-Step Guide

- 7 Investing Mistakes Beginners Should Avoid

- How to Build Your First Investment Portfolio

This article is for informational and educational purposes only and does not constitute financial advice. Historical returns referenced are based on long-term averages and are not guaranteed. No affiliate relationships are currently in place for any platforms, tools, or funds mentioned in this post. Always consult a qualified financial professional before making investment decisions.