Most people think passive income requires something big.

A business. A rental property. A system that takes years to build.

But there’s a simpler starting point that most beginners overlook entirely.

Dividend ETFs.

Not because they make you rich overnight. But because they do something far more valuable – they create a system that generates income while you sleep, scales as you add to it, and requires almost no active management once it’s set up.

This guide explains exactly how that system works, which ETFs are worth considering in 2026, and how to build it even if you’re starting with a small amount of money.

WHAT IS PASSIVE INCOME FROM ETFS – AND HOW DOES IT ACTUALLY WORK?

Passive income from ETFs works through dividends.

When companies generate profits, some of them distribute a portion of those profits to shareholders. An ETF that focuses on dividend-paying companies collects those distributions and passes them on to you – the investor.

The process looks like this:

- You invest in a dividend ETF

- The ETF holds dozens or hundreds of dividend-paying companies

- Those companies pay dividends quarterly or monthly

- The ETF distributes those payments to you as income

- You can either withdraw that income or reinvest it to grow your position

What makes this passive is that you don’t have to do anything after the initial investment. The income arrives automatically, on a regular schedule, without any effort on your part.

If you’re still getting familiar with how ETFs work in general, understanding the basics in Investing for Beginners: The Complete Guide to Building Wealth in 2026 will give you the foundation you need before going deeper into income strategies.

WHY DIVIDEND ETFs ARE IDEAL FOR BEGINNERS

There are many ways to generate passive income. But dividend ETFs have specific advantages that make them particularly well-suited for people who are just starting out.

Diversification by default.

When you buy a single dividend ETF, you’re not betting on one company. You’re spreading your investment across dozens or hundreds of them. If one company cuts its dividend or declines in value, the impact on your overall income is minimal.

For a deeper look at why this matters,

What Is Diversification in Investing? The Smart Way to Reduce Risk breaks down exactly how spreading your investments protects your portfolio over time.

Low maintenance.

You don’t need to analyze individual stocks, monitor earnings reports, or make regular decisions. The ETF manages the portfolio for you.

Scalable from any starting point.

You don’t need $10,000 or $50,000 to begin. Many platforms allow you to invest in fractional shares, meaning you can start with $50, $100, or $500 and build from there. If you’re working with a limited starting amount,

How to Start Investing With $500 outlines a practical approach for getting started without

waiting until you have “enough.”

Reinvestment is automatic.

Most brokerages offer automatic dividend reinvestment (DRIP). This means your income is used to purchase more shares, which then generate more income – a compounding cycle that builds momentum over time.

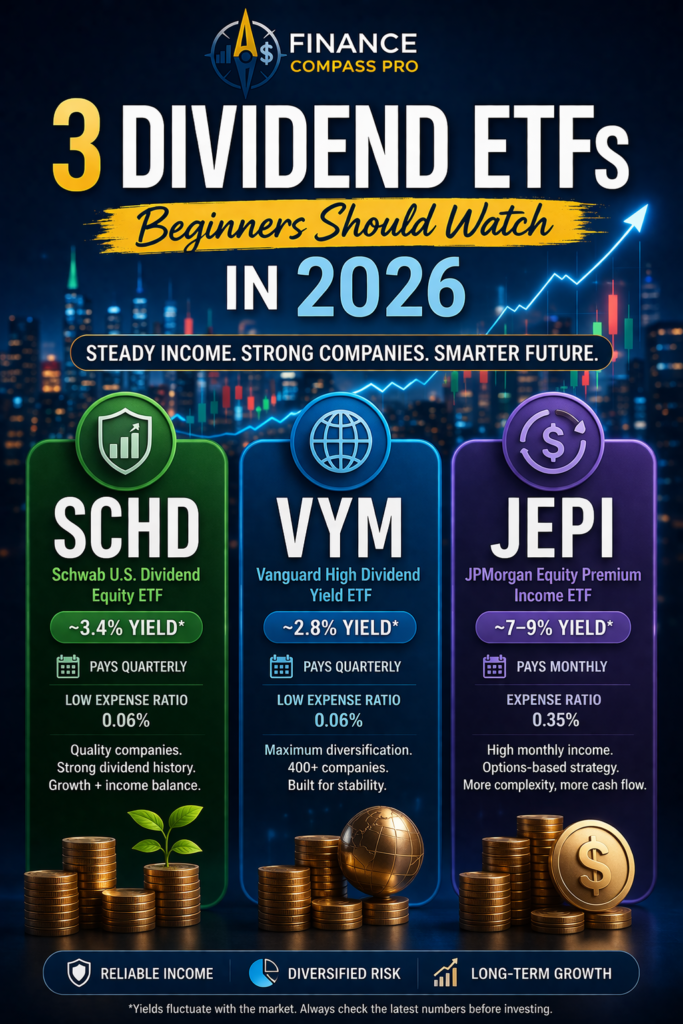

3 DIVIDEND ETFs WORTH CONSIDERING IN 2026

Not all ETFs are the same. For income-focused investing, here are three of the most widely respected options among beginner and intermediate investors.

| ETF | Yield (Approx.) | Payment Frequency | Expense Ratio | Best For |

|---|---|---|---|---|

| SCHD – Schwab US Dividend Equity | ~3.4% | Quarterly | 0.06% | Income + growth balance, strong dividend history |

| VYM – Vanguard High Dividend Yield | ~2.8% | Quarterly | 0.06% | Conservative investors, maximum diversification (400+ companies) |

| JEPI – JPMorgan Equity Premium Income | ~7-9% | Monthly | 0.35% | Maximum current cash flow, accepts more complexity |

Dividend yields fluctuate with market conditions. Always verify current figures directly on your brokerage or the fund provider’s website before investing.

If you’re still deciding whether ETFs are the right vehicle for you compared to individual stocks,

Stocks vs ETFs for Beginners: Which Investment Is Better for You?

walks through the key differences so you can make a more informed choice.

JEPI pays dividends monthly rather than quarterly, which is appealing for investors who want more frequent income. The higher yield comes with slightly more complexity, but for income-focused beginners, it’s worth understanding.

Note: Dividend yields fluctuate with market conditions. Always verify current figures before making any investment decisions.

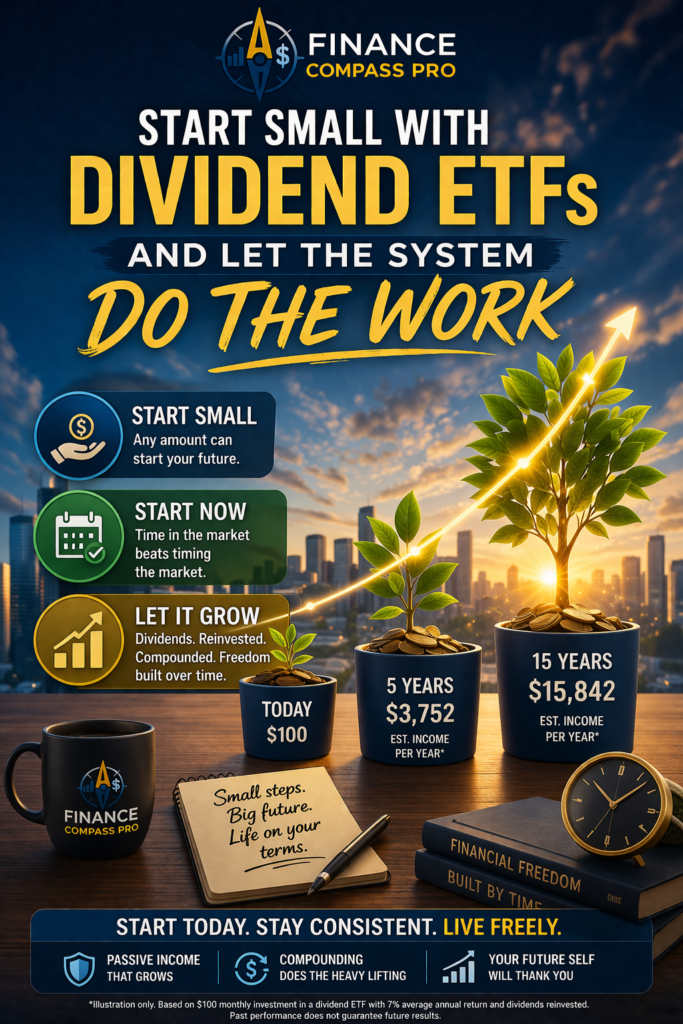

WHAT DOES THE INCOME ACTUALLY LOOK LIKE? A SIMPLE ILLUSTRATION

Numbers make this real. Here’s a simple illustration of what dividend income can look like over time, using SCHD as an example with an assumed 3.4% annual yield and 8% average annual growth (including reinvestment).

| Starting Amount | Year 1 Income | Year 5 Income | Year 10 Income |

|---|---|---|---|

| $1,000 | $34 | $50 | $73 |

| $5,000 | $170 | $249 | $367 |

| $10,000 | $340 | $499 | $735 |

| $25,000 | $850 | $1,247 | $1,837 |

These are not guarantees – they are illustrations based on historical averages.

But they demonstrate a key principle: the longer you stay invested, the more your income grows without any additional effort.

This is the compounding effect in action. Reinvested dividends purchase more shares. More shares generate more dividends. The cycle builds on itself quietly, in the background, while you focus on other things.

THE INCOME AND GROWTH BALANCE MOST BEGINNERS GET WRONG

There’s a common mistake beginners make when they first discover dividend investing.

They focus entirely on yield.

They search for the highest dividend percentage they can find and put everything there, assuming more yield equals more income.

In reality, high-yield investments often come with higher risk, lower growth, or both. A company paying a 12% dividend yield is often doing so because its stock price has fallen – which means the total value of your investment may be

declining even as the income arrives.

The most effective approach for long-term wealth building balances both income and growth. This is one of the core principles covered in

The 5 Pillars of Smart Investing Every Beginner Should Understand

and understanding it early saves most beginners from making expensive mistakes.

A well-structured starting portfolio – as outlined in How to Build Your First Investment Portfolio

allows you to generate current income while still participating in the long-term appreciation of the market.

That balance is what makes dividend investing sustainable rather than just temporarily high-paying.

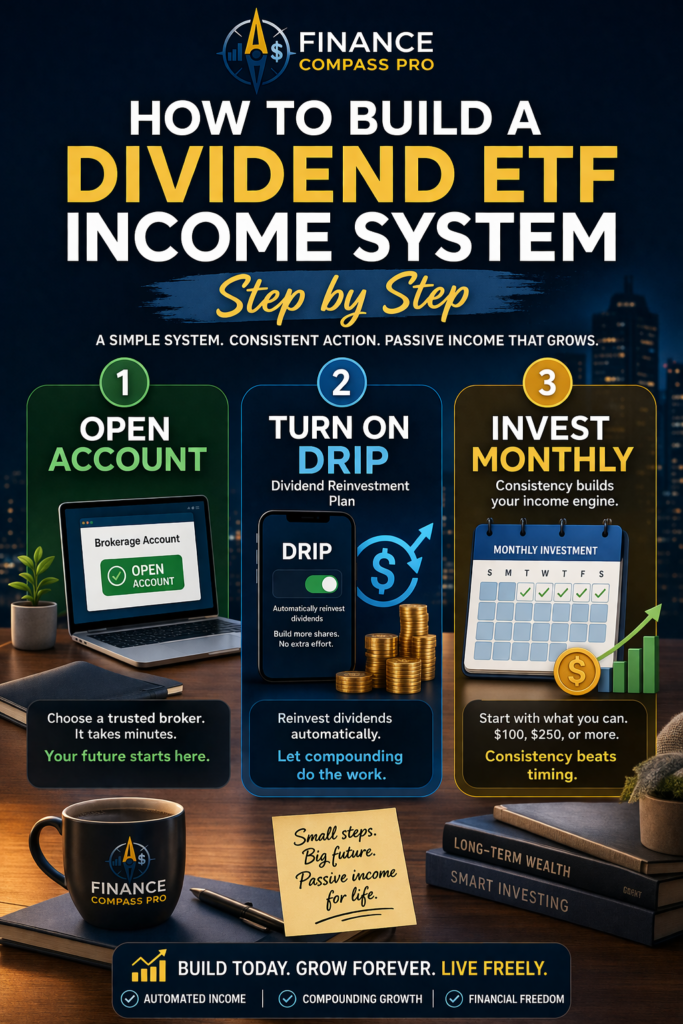

HOW TO START BUILDING YOUR DIVIDEND ETF INCOME SYSTEM

Getting started is simpler than most people expect.

Step 1: Open a brokerage account

Choose a platform that offers commission-free ETF trading and automatic dividend reinvestment. Most major platforms offer both.

Step 2: Decide on your starting amount

There is no minimum that makes this “worth it.” Starting with $100 matters less than starting consistently. The habit of investing regularly is more valuable than the initial amount. If you’re starting small,

How to Start Investing With $100: A Beginner’s Step-by-Step Guide gives you a clear path from your first dollar.

Step 3: Select one or two dividend ETFs to start

Trying to build a complex portfolio from day one adds unnecessary complexity.

Start simple. SCHD or VYM alone is a reasonable starting point for most beginners.

To understand how these fit into a broader strategy, reviewing

Investing for Beginners: The Complete Guide to Building Wealth in 2026 first will help you make a more confident decision.

Step 4: Enable automatic dividend reinvestment (DRIP)

This single setting transforms your dividends from occasional income into a compounding growth engine. Set it once and forget it.

Step 5: Add to your position regularly

Monthly contributions – even small ones – accelerate the compounding process significantly. Consistency matters more than timing. If you’re not sure how to fit this into your current finances, How to Build a Simple Budget That

Actually Works in 2026 helps you find the space in your monthly cash flow to start contributing regularly.

WHERE PASSIVE INCOME ACTUALLY COMES FROM

There’s a shift that happens when people begin to understand dividend investing.

At first, passive income feels like a concept – something that exists for other people, in different financial situations.

Then, when the first dividend arrives, something changes.

It’s often a small amount. A few dollars. Maybe less.

But it’s income that arrived without effort. Income that will arrive again next quarter, and the one after that, without you doing anything.

That experience changes how people think about money.

Because it makes the system tangible.

Reinvested dividends generate more income. More income creates more flexibility.

And that flexibility, over time, becomes something meaningful.

This is where passive income stops being an idea.

And starts becoming a system.

START SMALL. START NOW. LET THE SYSTEM DO THE WORK.

The most common mistake people make with passive income is waiting.

Waiting until they have more money. Waiting until they understand it better.

Waiting for the right moment.

But passive income systems are built by starting, not by waiting.

Your action step for today:

Look up SCHD or VYM on your brokerage platform. See what a $100 or $500 investment would look like. Run the numbers. Make it real.

The system doesn’t start until you do.

This article is for informational and educational purposes only and does not constitute financial advice. ETF yields and performance figures referenced are based on historical averages and are not guaranteed. No affiliate relationships are currently in place for any platforms, tools, or funds mentioned in this post. Always consult a qualified financial professional before making investment decisions.

passive income, etf investing, dividend etf, reit etf, income investing, financial freedom, cash flow investing, beginner investing, portfolio strategy

Pingback: How to Build Your First Investment Portfolio: A Beginner’s Step-by-Step GuideHow to Build Your First Investment Portfolio -

Pingback: What Is an ETF and How Does It Work? A Beginner’s Guide to Smart InvestingWhat Is an ETF and How Does It Work? A Beginner’s Guide to Smart Investing -

Pingback: Psychological Spending Triggers That Make You Spend Without Realizing ItPsychological Spending Triggers That Make You Spend Without Realizing It -

Pingback: Passive Income With $1,000: Realistic Strategies That Actually Work in 2026Passive Income With $1,000: Realistic Strategies That Actually Work in 2026 -