Tags: #ETF portfolio #beginner investing #index fund strategy #passive investing #build wealth

When people first start investing, the biggest obstacle isn’t money.

It’s uncertainty.

Too many options. Too many opinions. Too much noise. And in that environment, doing nothing often feels safer than making the wrong decision.

But here’s what most beginners don’t realize.

You don’t need dozens of stocks. You don’t need a complex strategy. You don’t need to constantly watch the market. What you need is a simple structure that works – consistently, over time.

That structure is a 3 ETF portfolio. And it’s been quietly building wealth for everyday investors for decades.

→ What Is an ETF and How Does It Work

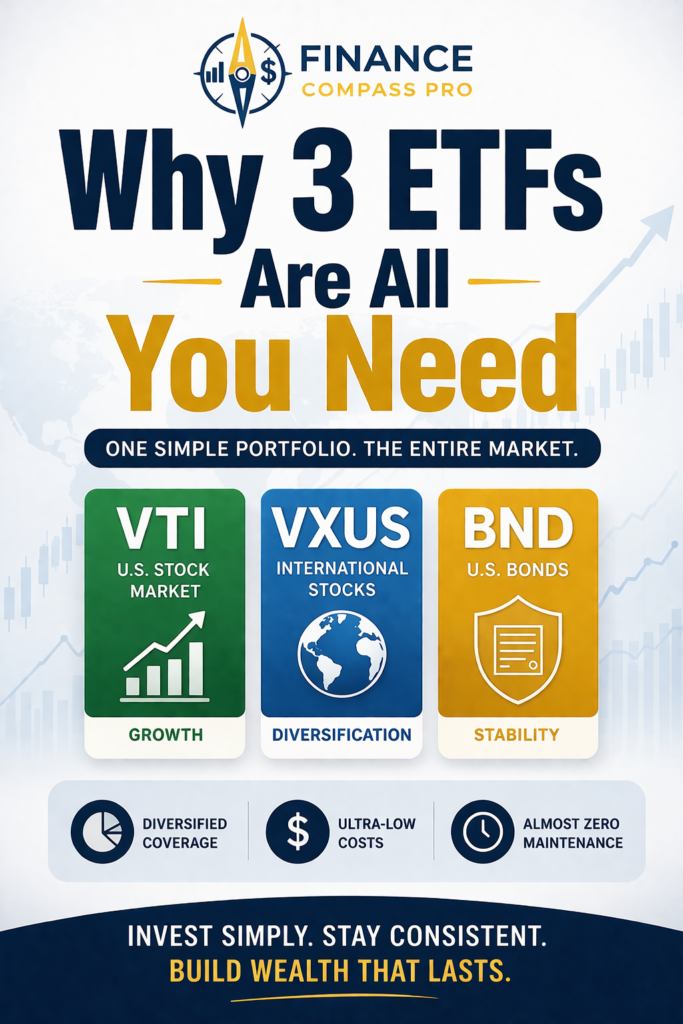

Why Three ETFs Are All You Need

At its core, this strategy is built on one simple idea.

Instead of trying to pick winners, you own the market itself.

A broad U.S. market ETF gives you exposure to overall economic growth. An international ETF expands that exposure beyond a single country. And a bond ETF adds stability – smoothing out volatility when markets get rough.

Individually, each piece serves a purpose. Together, they cover nearly every investable asset class on the planet. You’re not missing anything important.

⚡ KEY INSIGHT

Most beginners focus on maximizing returns. But sustainable investing is about managing risk while staying invested long enough to let compounding do its work.

That balance is exactly what a simple portfolio structure provides.

The result is a portfolio that’s genuinely diversified, incredibly low-cost, and almost entirely automatic.

Tags: #3 ETF portfolio #passive income investing #ETF strategy #index investing #long term wealth

The 3 ETFs – What Each One Does

Here’s the core of the strategy. Three funds. One clear purpose for each.

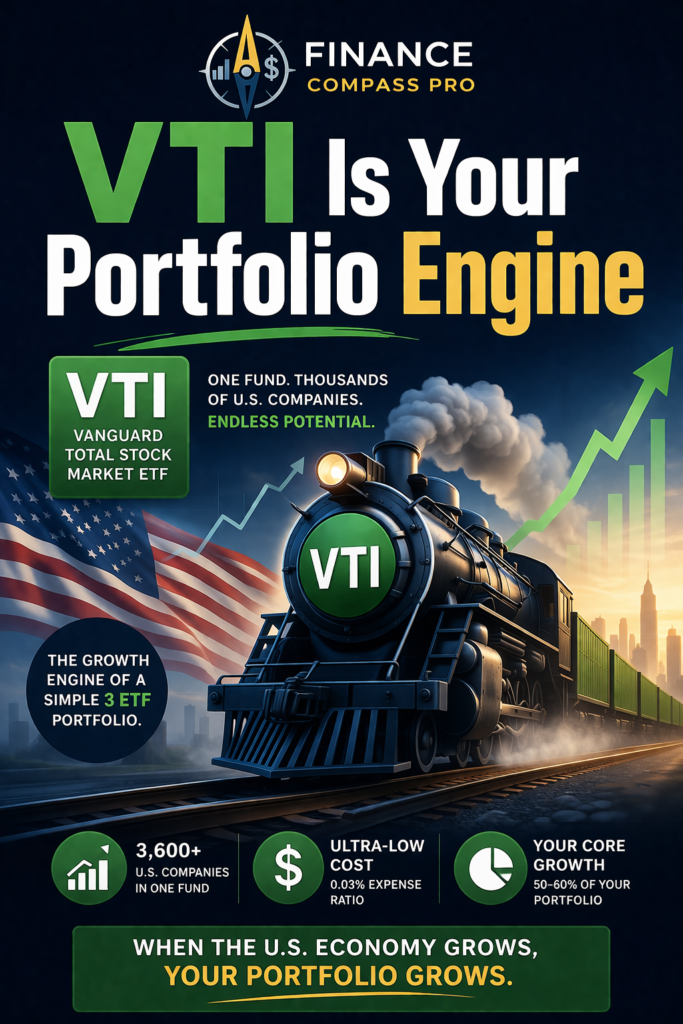

ETF 01 – Broad U.S. Market ETF

This is your engine.

A total market or S&P 500 ETF gives you ownership of hundreds – or thousands – of companies in a single investment. When the U.S. economy grows, your portfolio grows with it.

The most widely used option is VTI (Vanguard Total Stock Market ETF), which holds over 3,600 U.S. companies across every size and sector. Its expense ratio is just 0.03% annually – meaning for every $10,000 invested, you pay $3 per

year in fees.

For Fidelity users, FZROX (Fidelity ZERO Total Market Index Fund) takes this even further – a 0.00% expense ratio with zero minimum investment.

This ETF typically makes up 50 to 60 percent of a beginner’s portfolio.

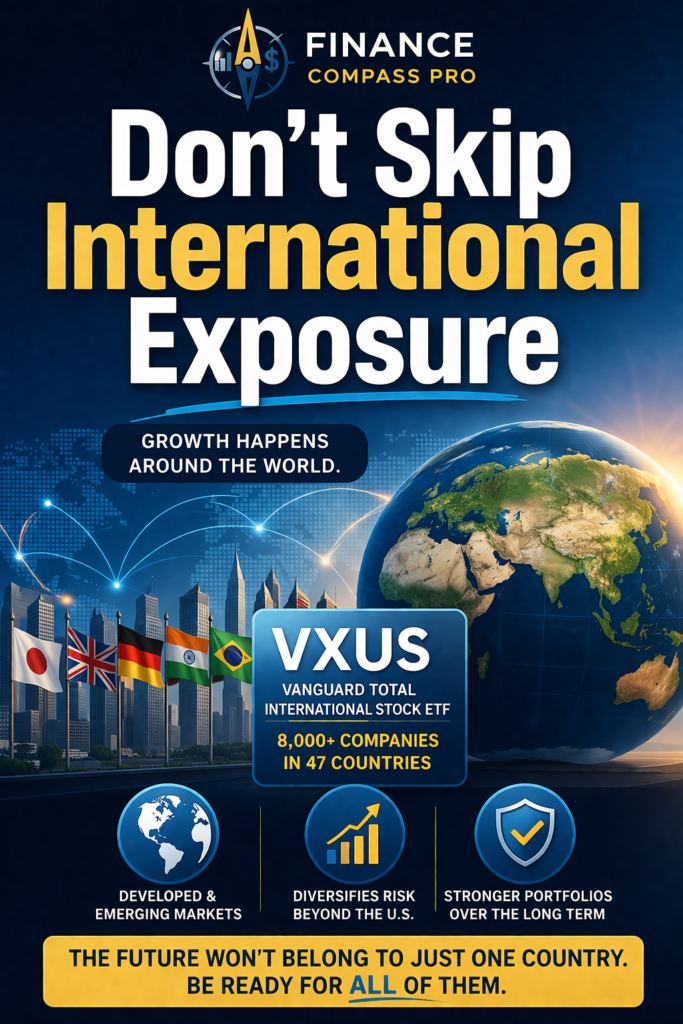

ETF 02 – International ETF

No single economy grows in a straight line.

An international ETF spreads your exposure across developed and emerging markets outside the U.S. – countries like Japan, the U.K., Germany, and South Korea, as well as faster-growing markets in Asia and Latin America.

The standard choice here is VXUS (Vanguard Total International Stock ETF), which covers over 8,000 companies across 47 countries. Expense ratio: 0.05%.

Why does this matter? Over different decades, international markets have significantly outperformed the U.S. – and vice versa. Owning both removes the guesswork of which region will lead next.

This ETF typically accounts for 20 to 30 percent of your total allocation.

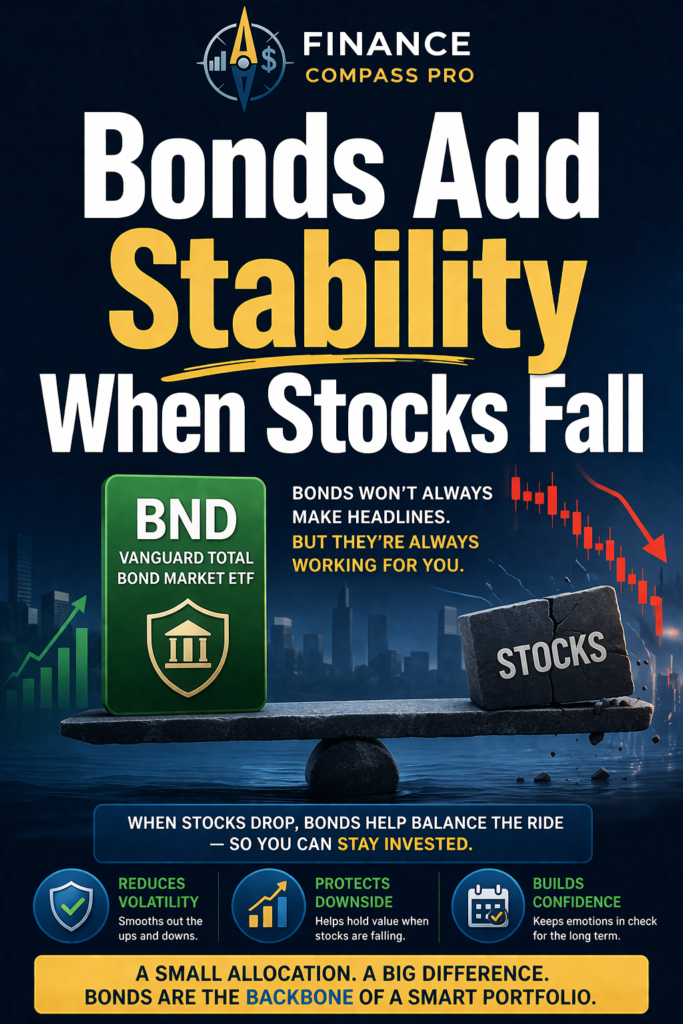

ETF 03 – Bond ETF

Bonds don’t grow as fast as stocks. That’s not the point.

Their job is to hold their value – or even rise – when stock markets fall. When equities dropped 34% during the COVID crash of early 2020, bond funds largely held steady. That cushion is what keeps beginners from panic-selling at the

worst possible moment.

BND (Vanguard Total Bond Market ETF) holds over 10,000 U.S. government and corporate bonds. Expense ratio: 0.03%.

For most young investors, a 10% bond allocation is enough. As you approach retirement, that number typically grows.

→ Which Is Better for Beginners ETFs or Stocks

Tags: #3 ETF portfolio #passive income investing #ETF strategy #index investing #long term wealth

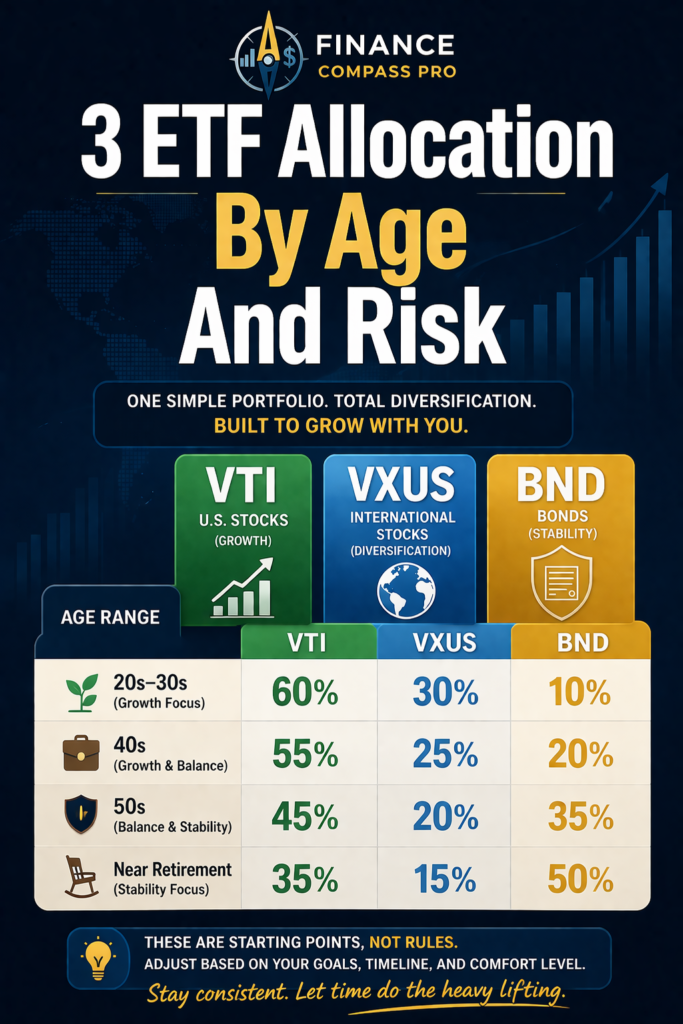

A Simple Allocation Table

Here’s how a typical 3 ETF portfolio might look at different life stages.

| Age Range | VTI (U.S.) | VXUS (Intl) | BND (Bonds) |

|---|---|---|---|

| 20s–30s | 60% | 30% | 10% |

| 40s | 55% | 25% | 20% |

| 50s | 45% | 20% | 35% |

| Near Retire | 35% | 15% | 50% |

These aren’t rigid rules. They’re starting points.

Your allocation should reflect your risk tolerance – not just your age. Someone in their 40s with a stable income and strong emergency fund may comfortably hold more in equities. Someone in their 30s who lost sleep during market downturns might prefer a more conservative split.

The key is choosing an allocation you can actually stick with.

Why Simplicity Is the Strategy

This is where many beginners go wrong.

They overcomplicate things. They add more funds to feel more diversified. They chase recent top-performers. They react to headlines.

But the investors who succeed long-term tend to do the opposite. They simplify, stay consistent, and make as few decisions as possible.

That’s not “basic” investing. That’s disciplined investing.

THE PRINCIPLE THAT CHANGES EVERYTHING

“The goal isn’t to build the perfect portfolio. It’s to build one you can stick with.” Because consistency – more than fund selection or market timing – is what turns investing into long-term wealth.

With a 3 ETF portfolio, there are almost no decisions to make after setup. No individual stocks to research. No quarterly rebalancing obsession. No noise to react to.

That psychological simplicity is an underrated advantage.

Tags: #3 ETF portfolio #passive income investing #ETF strategy #index investing #long term wealth

How to Stay Consistent With This Strategy

The second major advantage of this approach is how naturally it supports regular, automatic investing.

Instead of trying to time the market, you invest a fixed amount on a fixed schedule – every month, regardless of what markets are doing. This is the core principle behind dollar-cost averaging.

When prices are high, your fixed contribution buys fewer shares. When prices drop, it buys more. Over time, this smooths out your average cost and removes emotion from the equation entirely.

→ What Is Dollar-Cost Averaging and Why Smart Investors Use It

The math behind this is compelling. A $500 monthly contribution into a simple 3 ETF portfolio, started at age 25 and held until 65, grows to approximately $1.3 million at a 7% average annual return – before any salary increases or additional contributions.

The strategy doesn’t change. The contributions just continue.

Tags: #ETF investing #beginner portfolio #how to invest #simple investing strategy #wealth building

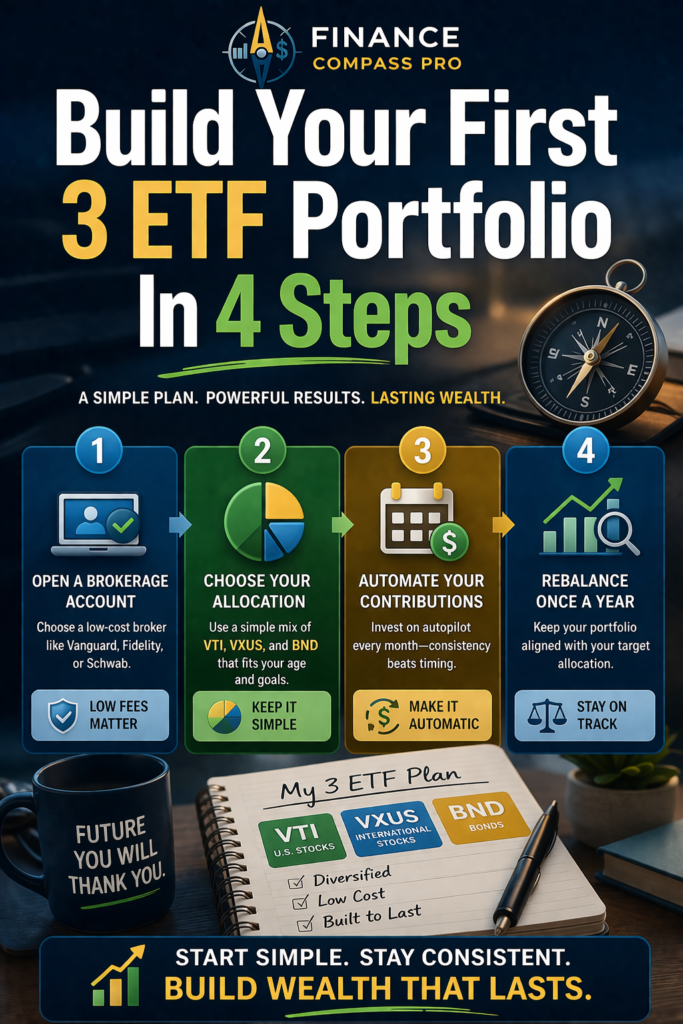

How to Build Your First 3 ETF Portfolio

Getting started takes four steps. Most people can complete all of them in under an hour.

Step 1: Open a Brokerage Account

Before selecting ETFs, you need an account. Look for a platform with zero commission trades, no account minimums, and automatic investment options.

Fidelity and Charles Schwab are consistently recommended for beginners because of their $0 minimums, robust educational resources, and automatic investing features. Both allow fractional shares, meaning you can start with as little as $1.

Step 2: Choose Your Allocation

A standard beginner allocation: 60% VTI / 30% VXUS / 10% BND.

If you’re newer to investing and concerned about volatility, shift slightly more toward bonds – say, 55% / 25% / 20%. If you’re young, have a long horizon, and can tolerate short-term swings, stay heavier in equities.

Pick a ratio. Write it down. Stick to it.

Step 3: Set Up Automatic Contributions

Decide on a fixed monthly amount – even $100 is a meaningful start. Then automate it. Most brokerages allow automatic monthly purchases directly into your chosen ETFs.

The less you have to consciously decide each month, the more consistent you’ll be. Automation removes willpower from the equation.

Step 4: Rebalance Once a Year – Not More

Over time, one ETF will grow faster than the others and shift your allocation off target. An annual rebalance – selling a small amount of what grew, buying a small amount of what didn’t – keeps your risk level where you intended it.

Once per year is sufficient. More frequent rebalancing adds transaction costs and behavioral risk without meaningfully improving returns.

→ How to Build Your First Investment Portfolio

The Real Advantage of This Approach

At the end of the day, the 3 ETF portfolio works not because it’s the most sophisticated strategy – but because it’s one that any beginner can start with, stick to, and build on.

It removes the paralysis of too many choices.

It reduces the emotional temptation to react to short-term noise.

It gives your money a clear, consistent direction – backed by decades of evidence that simple, low-cost index investing outperforms most actively managed alternatives over time.

That’s not a compromise. That’s the strategy.

→ Investing for Beginners: The Complete Guide to Building Wealth in 2026

RELATED POSTS SECTION

[Beginner] Investing for Beginners: The Complete Guide to Building Wealth in 2026

[ETF] What Is an ETF and How Does It Work? A Beginner’s Guide to Smart Investing

[ETF] What Is an ETF and How Does It Work

[Strategy] What Is Dollar-Cost Averaging and Why Smart Investors Use It

[Comparison] Which Is Better for Beginners ETFs or Stocks

[Passive Income] Passive Income From ETFs: Build Cash Flow Without Managing Individual Stocks

This article is for informational and educational purposes only and does not constitute financial advice. No affiliate relationships are currently in place for any platforms or tools mentioned in this post. Past performance does not guarantee future results. Always consult a qualified financial professional before making investment decisions.

Pingback: Which Is Better for Beginners ETFs or Stocks -

Pingback: How to Build Passive Income With Small Capital (Even If You're Starting From Scratch)How to Build Passive Income With Small Capital (Even If You're Starting From Scratch) -

Pingback: Investing for Beginners: The Complete Guide to Building Wealth in 2026Investing for Beginners: The Complete Guide to Building Wealth in 2026 -