Most financial conversations focus on how to earn more.

More income, better salary negotiations, side hustles – the assumption being that the path to financial security runs through a bigger paycheck.

But there’s a parallel conversation that gets far less attention: how much you’re quietly losing on the other side of the ledger.

And one of the biggest drivers of that silent loss is a three-digit number most people barely think about until they need a loan.

Your credit score doesn’t make headlines. It doesn’t feel like it’s doing anything on an ordinary Tuesday. But the moment you borrow money – for a car, a home, a business, or a personal expense – it steps out of the background and starts determining the terms under which you live your financial life.

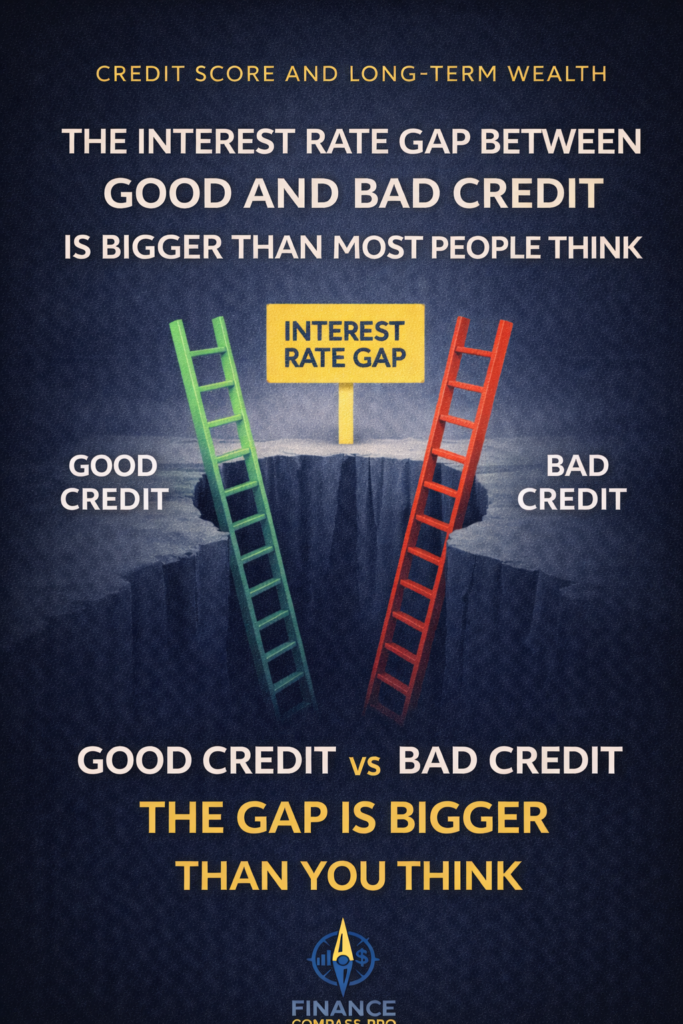

The difference between a good credit score and a poor one isn’t just a few percentage points on an interest rate. Over the course of a mortgage, a car loan, or years of credit card balances, it can add up to tens of thousands of dollars – money that either stays in your pocket or quietly flows to lenders.

This article makes that cost visible. Because once you see the real numbers, the case for taking your credit score seriously becomes impossible to ignore.

What Lenders Actually See When They Check Your Score

When you apply for any kind of credit – a mortgage, a car loan, a personal loan, or even a credit card – the lender pulls your credit report and score.

What they’re looking for is risk.

They’re not evaluating your character, your work ethic, or your intentions. They’re asking one narrow question: based on this person’s borrowing history, how likely are they to repay this debt on time?

Your credit score is their answer, compressed into a number typically ranging from 300 to 850.

The higher the score, the lower the perceived risk. And lower perceived risk translates directly into lower interest rates – because the lender feels confident enough in repayment that they don’t need to charge a large premium to protect themselves.

The lower the score, the higher the perceived risk. Lenders compensate by charging more. Not as punishment, but as a calculated hedge: if a certain percentage of lower-score borrowers default, higher rates on all of them need to cover those losses.

This mechanism is entirely predictable. And that predictability means improving your score has a direct, calculable effect on your borrowing costs.

Credit Score Ranges and What They Mean to Lenders

| Score Range | Rating | Lender’s Perception | Typical Access |

|---|---|---|---|

| 800–850 | Exceptional | Extremely low risk | Best rates available |

| 740–799 | Very Good | Low risk | Competitive rates |

| 670–739 | Good | Acceptable risk | Standard rates |

| 580–669 | Fair | Elevated risk | Higher rates, limited options |

| Below 580 | Poor | High risk | Highest rates or denied |

Ranges based on FICO scoring model. Individual lender criteria vary.

The Real Dollar Cost of a Lower Credit Score

The abstract explanation is one thing. The numbers are another.

Let’s look at what credit score differences actually cost on two of the most common types of borrowing.

Mortgage: $350,000 30-Year Fixed Loan

| Credit Score | Estimated Rate | Monthly Payment | Total Interest Paid | Extra Cost vs. Top Tier |

|---|---|---|---|---|

| 760–850 | ~6.5% | ~$2,212 | ~$446,300 | — |

| 700–759 | ~6.75% | ~$2,270 | ~$467,200 | +$20,900 |

| 640–699 | ~7.25% | ~$2,389 | ~$510,000 | +$63,700 |

| 580–639 | ~8.0% | ~$2,568 | ~$573,500 | +$127,200 |

Rates are illustrative estimates based on typical lender spreads. Actual rates vary by lender, loan type, and market conditions.

Auto Loan: $35,000 60-Month Loan

| Credit Score | Estimated Rate | Monthly Payment | Total Interest Paid | Extra Cost vs. Top Tier |

|---|---|---|---|---|

| 720+ (Super Prime) | ~5.5% | ~$670 | ~$5,200 | — |

| 660–719 (Prime) | ~7.5% | ~$700 | ~$7,000 | +$1,800 |

| 620–659 (Near Prime) | ~10.5% | ~$751 | ~$10,060 | +$4,860 |

| Below 620 (Subprime) | ~14.0% | ~$814 | ~$13,840 | +$8,640 |

Estimates based on typical market spreads for auto financing. Rates vary by lender and current market conditions.

The pattern is consistent across every type of borrowing. A borrower with an exceptional credit score and a borrower with a poor credit score can finance the exact same asset, make payments for the same number of years, and end up in completely different financial positions – not because of anything they did during the loan period, but because of the rate they were assigned at the start.

“Two borrowers. Same house. Same loan amount. One pays $127,000 more over 30 years – because of a number they barely thought about.”

How Interest Rate Differences Compound Over Time

The tables above show total interest paid – but there’s a second-order effect that the numbers don’t fully capture.

Every extra dollar going toward interest is a dollar not going toward something else.

For someone paying an extra $356/month on their mortgage compared to a higher-score borrower (the difference between the top and second-lowest tier in the table above), that gap represents:

- $356/month that could instead go into an investment account

- At 7% average annual return, $356/month invested over 30 years grows to approximately $435,000

So the true cost of a lower credit score isn’t just the extra interest paid. It’s also the wealth that never got built because that money was redirected to lenders instead of investments.

This is the compounding effect working in the wrong direction – and it’s why the credit score conversation belongs in the same category as investing, saving, and budgeting when it comes to long-term financial planning.

Beyond Mortgages and Auto Loans: Where Else Your Score Matters

Most people understand that credit scores affect loan rates. Fewer realize how many other financial decisions your score quietly influences.

Credit cards. The interest rate (APR) on your credit card is directly tied to your credit profile. Carrying a balance on a card with a 24% APR versus a 16% APR is a significant cost difference on the same debt.

Renting an apartment. Most landlords and property management companies run credit checks as part of their application process. A lower score can result in denial, a required co-signer, or a larger security deposit.

Insurance premiums. In most U.S. states, auto and homeowners insurance companies use credit-based insurance scores – closely related to your credit score – to help set premiums. Lower scores often correlate with higher insurance costs, even for people with clean driving records.

Employment. Some employers, particularly for roles involving financial responsibility, run credit checks as part of background screening. This is not universal, but it is common enough to be worth knowing.

Starting a business. Business financing, especially early-stage loans and credit lines, often incorporates the owner’s personal credit score when business credit history is thin.

“Your credit score isn’t just a loan metric. It’s a number that quietly shapes your rent, your insurance, your job prospects, and your ability to build wealth.”

Why Improving Your Score Changes the Structure – Not Just the Number

This is the insight most credit score articles miss.

Improving your credit score isn’t a cosmetic change. It doesn’t just make you feel better about a number on a report. It restructures the cost of your financial life going forward.

Every future loan you take, every credit card you open, every rental application you submit – all of these operate under different terms once your score improves. The rules you play by change.

Think of it as adjusting the settings on a game before you start playing. A higher credit score means lower friction, lower costs, and better access to the financial tools that make wealth-building faster. A lower score means higher friction, higher costs, and fewer options – not forever, but for as long as you leave it unchanged.

The good news is that credit scores respond to behavior. They are not permanent judgments. They are dynamic calculations based on what you’re doing now and what you’ve done recently – and that means they can be improved deliberately.

Where to Go From Here

If your credit score is lower than you’d like, the starting point is understanding what’s actually driving it.

Payment history is the single largest factor – accounting for roughly 35% of your FICO score. A pattern of on-time payments, maintained consistently, is the most reliable way to build score over time.

Credit utilization – the percentage of your available credit you’re currently using – is the second largest factor at around 30%. Keeping balances low relative to your credit limits has a direct and often fast impact on your score.

Other factors like length of credit history, credit mix, and recent applications make up the rest.

📌 Related reading: How to Improve Your Credit Score Fast in 30 Days – The specific, actionable steps to start moving your score immediately.

📌 Related reading: What Is a Credit Score? Everything Beginners Need to Know – A deeper look at how each factor is weighted and what changes produce the fastest results.

Final Thoughts: Your Credit Score Is Leverage

The framing most people use for credit scores is defensive – something to maintain so you don’t get denied for things.

A better framing is offensive.

A strong credit score is financial leverage. It reduces the cost of capital, which is one of the most powerful inputs in any wealth-building strategy. Lower borrowing costs mean more of your income stays available for saving and investing. More saving and investing, compounded over time, is how financial security gets built.

You don’t need to obsess over your score. But you do need to take it seriously – because the interest rate gap between a 580 and a 760 is not a minor inconvenience. Over the course of a financial life, it is a material difference in wealth.

Fix the structure first. Everything built on top of it becomes more efficient.

You Might Also Like:

- How to Improve Your Credit Score Fast in 30 Days

- What Is a Credit Score? Everything Beginners Need to Know

- 7 Simple Money Habits That Will Transform Your Finances

- 7 Investing Mistakes Beginners Make (And How to Fix Them)

- How to Build Your First Investment Portfolio

- What Is an Index Fund? The Beginner’s Complete Guide

- How to Start Investing With $500 – A Beginner’s Guide

This article is for informational and educational purposes only and does not constitute financial advice. Historical returns referenced are based on long-term averages and are not guaranteed. No affiliate relationships are currently in place for any platforms, tools, or funds mentioned in this post. Always consult a qualified financial professional before making investment decisions.

Pingback: 3 Reasons Why Your Credit Score Matters More Than You Think3 Reasons Why Your Credit Score Matters More Than You Think -

Pingback: Smart Credit & Wealth Planning: Strategies for Long-term Prosperity -

Pingback: How to Improve Your Credit Score Fast in 30 DaysHow to Improve Your Credit Score Fast in 30 Days -

Pingback: How to Improve Your Credit Score Step by StepHow to Improve Your Credit Score Step by Step -