Most people know they should be investing.

They’ve heard it enough times – from financial advice columns, from podcasts, from that one friend who won’t stop talking about their portfolio. The message is consistent: start early, invest regularly, let your money grow.

And yet, most beginners don’t start. Not because they lack the intention. Because they don’t know where to begin – and the sheer volume of conflicting information makes starting feel riskier than waiting.

That hesitation is understandable. But it’s also expensive.

“The barrier to investing isn’t knowledge. It’s the feeling that you need more knowledge before you’re allowed to start.”

This guide exists to remove that barrier. Not by overwhelming you with strategy, but by giving you a clear, honest framework for how investing actually works – and what to do first.

What Investing Actually Is (And What It Isn’t)

Before tactics, before fund selection, before any of the specific decisions that feel overwhelming at the start – it helps to be clear about what investing actually means.

Investing is not predicting the market. It’s not finding the perfect stock before everyone else does. It’s not a form of gambling, and it’s not reserved for people with finance degrees or large amounts of capital.

Investing is the process of putting your money into assets that grow in value over time – and allowing that growth to compound into something meaningful.

That’s it.

The complexity that surrounds investing – the terminology, the strategies, the endless debate between approaches – is largely noise layered on top of a simple core process. And for most beginners, the noise is what causes paralysis.

Here’s what the research consistently shows: the investors who build the most wealth over time are rarely the ones with the most sophisticated strategies. They’re the ones who started early, stayed consistent, and kept their approach simple enough to maintain through market conditions that made staying invested difficult.

Simplicity isn’t a compromise in investing. For most people, it’s a decisive advantage.

Why Most Beginners Never Start – And What Changes That

There’s a pattern in how most people approach investing for the first time.

They decide they want to start. They begin researching. They encounter terms they don’t fully understand, strategies that contradict each other, and warnings about risks they hadn’t considered. The research that was supposed to create confidence instead creates more uncertainty.

So they wait. For more clarity. For a better moment. For a level of understanding that will finally make the decision feel safe.

That level of understanding rarely arrives – because the information keeps expanding faster than confidence builds.

The reframe that actually moves people forward is this: you don’t need to understand everything before you start. You need to understand enough to take one concrete first step.

That first step, executed imperfectly, teaches you more than months of additional research. It makes the process real. It transforms investing from something you’re planning to do into something you’re already doing.

And for most beginners, starting with a small amount removes the pressure that makes that first step feel so significant. How to Start Investing With $100 walks through exactly how to build a real investment position from a modest starting point – one that teaches the process without requiring capital you can’t afford to commit.

The Foundation: What You’re Actually Investing In

Before choosing specific investments, it’s worth understanding the basic categories of assets available to you – and what each one is designed to do.

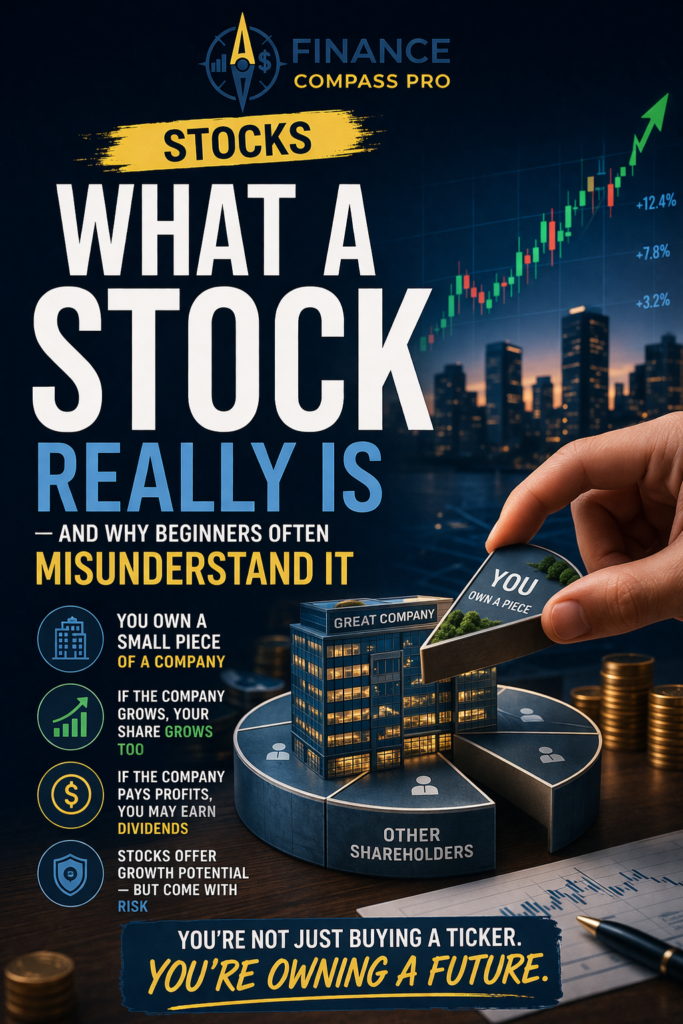

📈 Stocks

A stock represents a fractional ownership stake in a company. When you buy a share of stock, you own a small piece of that business. If the company grows and becomes more valuable, your stake becomes more valuable. If it struggles, your investment declines.

Individual stocks offer the highest potential returns – but also the highest risk. A single company’s performance is influenced by factors ranging from industry trends to management decisions to global economic conditions. Getting it right consistently requires significant research, ongoing attention, and emotional discipline that most beginners underestimate.

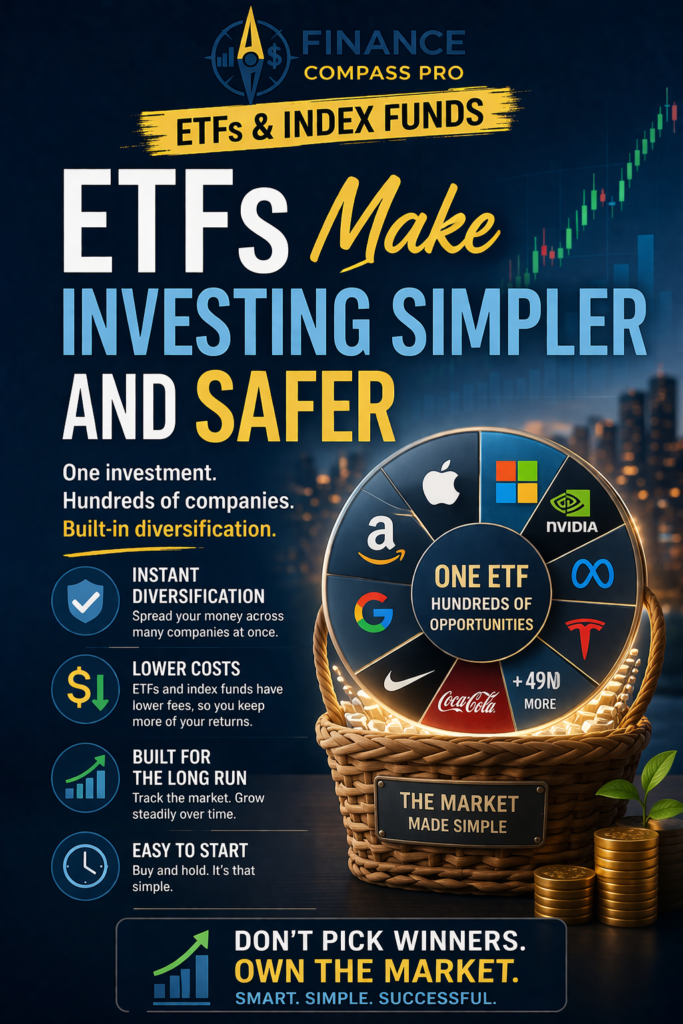

📊 ETFs and Index Funds

An ETF (Exchange-Traded Fund) holds a collection of investments – often dozens or hundreds of individual stocks – bundled into a single fund that trades like a stock. When you buy one share of an S&P 500 ETF, you’re effectively investing in 500 companies simultaneously.

This structure provides instant diversification. Instead of betting on a single company, you’re spreading your investment across the broader market. One company performing poorly doesn’t significantly impact your portfolio because it represents a small fraction of the whole.

For most beginners, ETFs and index funds are the most practical starting point – not because they’re a compromise, but because they offer broad exposure, low costs, and a level of simplicity that makes staying consistent significantly easier.

If you’re still deciding between individual stocks and funds, Stocks vs ETFs for Beginners breaks down the specific trade-offs – and helps you identify which approach matches your current experience level and investment goals.

🏦 Bonds

Bonds are loans made to governments or corporations in exchange for regular interest payments over a fixed period. They’re generally less volatile than stocks – and tend to move in the opposite direction, providing stability when equity markets decline.

For most beginners, bonds become relevant as a portfolio stabilizing element rather than a primary investment. The typical starting point is a predominantly equity-focused portfolio, with bonds added as your portfolio grows and your approach to risk management becomes more sophisticated.

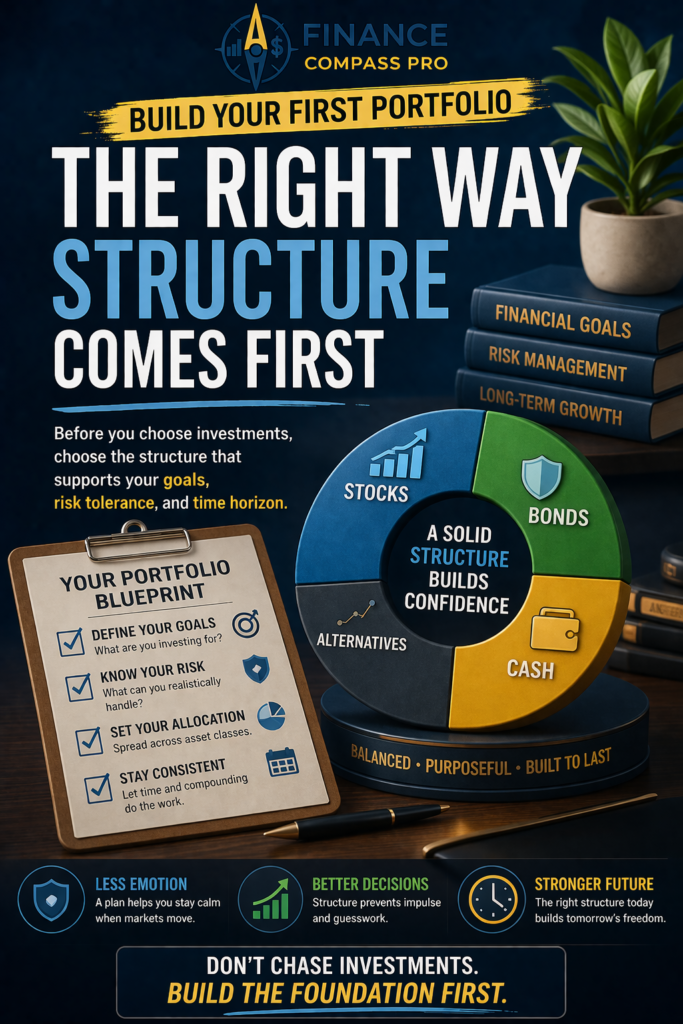

Building Your First Portfolio: Structure Before Selection

Here’s the mistake most beginners make.

They focus on selecting the best individual investments before establishing a structure for how those investments will work together.

The result is a portfolio built from a series of individual decisions rather than a coherent strategy. Some positions are short-term. Others are long-term. Some are high-risk speculations. Others are conservative holds. The whole doesn’t add up to a clear direction.

A structured approach works differently. Before selecting specific investments, you establish:

- What proportion of your portfolio will be in equities vs. bonds

- Whether you’re prioritizing growth, income, or a combination

- How you’ll respond when market conditions change

- When and how you’ll rebalance

That structure doesn’t need to be complex. For most beginners, a simple three-fund approach – a domestic equity fund, an international equity fund, and a bond fund – provides comprehensive diversification, low costs, and a clarity that’s easy to maintain over time.

The Simple 3 ETF Portfolio Strategy Most Beginners Should Start With walks through exactly how to build this foundation – including how to allocate between the three funds based on your timeline and risk tolerance.

And if you’re ready to think through the broader portfolio construction process, How to Build Your First Investment Portfolio covers the full framework for moving from individual fund selection to a coherent long-term structure.

The Timing Problem – And Why Consistency Solves It

One of the most persistent questions beginners face is deceptively simple: when should I invest?

The honest answer is that no one knows. Not professional investors. Not financial institutions with research teams and decades of data. Not the analysts who appear on financial news networks projecting market movements with apparent confidence.

Markets don’t move in predictable patterns. They’re influenced by economic data, geopolitical events, central bank decisions, and the collective psychology of millions of participants – all interacting in real time, in ways that no model fully captures.

Waiting for the right moment – for the market to dip to the perfect entry point, for conditions to feel sufficiently stable, for confidence to reach a level that justifies committing – produces one consistent outcome: delayed starting.

And delayed starting is expensive. Not dramatically, month to month. Enormously, over a decade.

The strategy that solves this isn’t sophisticated. It’s consistent investing at regular intervals, regardless of what markets are doing. When prices are high, your investment buys fewer shares. When prices are low, the same investment buys more. Over time, your average cost tends to be lower than the average price during the same period – without requiring you to identify the bottom.

This approach is called dollar-cost averaging, and it’s one of the most powerful tools available to individual investors – precisely because it requires no market prediction at all. What Is Dollar-Cost Averaging explains how it works in practice and why it consistently outperforms timing-based approaches for most long-term investors.

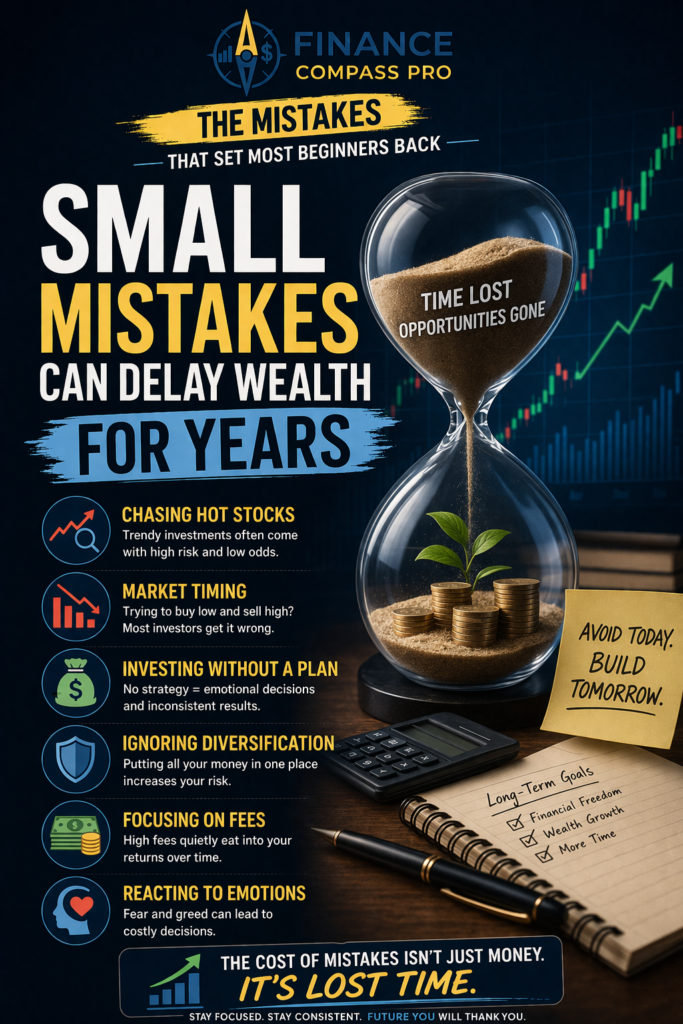

The Mistakes That Set Most Beginners Back

Every investor makes mistakes. That’s not pessimism – it’s an acknowledgment that investing involves decisions made under uncertainty, and uncertainty produces errors.

But most beginner mistakes aren’t random. They follow predictable patterns.

Overreacting to short-term volatility. Markets decline. Sometimes significantly. Investors who interpret those declines as signals to exit lock in losses that a diversified, patient approach would have recovered from. The data is consistent: investors who stay invested through downturns outperform investors who move to cash and attempt to time re-entry.

Overcomplicating the strategy. More complexity does not produce better results. A simple, low-cost, diversified portfolio maintained consistently outperforms a sophisticated tactical strategy maintained inconsistently. The simpler your approach, the easier it is to sustain through the conditions that test it.

Concentrating too early. Beginners frequently allocate too much to a single stock, sector, or theme because the return potential looks compelling. When that concentration underperforms – as single positions frequently do – the emotional and financial impact is disproportionate to what a diversified position would have produced.

Expecting too much too soon. Investing works over years and decades, not weeks and months. The investors who abandon their strategy because it hasn’t produced dramatic results in six months miss the compounding that becomes significant precisely because of the time they spent in the market consistently.

7 Investing Mistakes Beginners Make covers these patterns in detail – and more importantly, explains the structural adjustments that prevent them from recurring.

The Role of Compounding – And Why Starting Early Matters So Much

Here’s the mathematical reality that most beginners understand intellectually but rarely feel viscerally until years have passed.

Compounding means that your returns generate their own returns. The growth on your initial investment produces growth. The growth on that growth produces more growth. And so on, indefinitely.

In the early years, this feels underwhelming. The numbers are small. The progress feels invisible.

But compounding is not linear – it’s exponential. The same mechanism that produces modest results in years one through five produces dramatically larger results in years fifteen through twenty. The curve bends sharply upward – and it does so whether you’re watching or not.

The implication is simple: time in the market is more valuable than the amount you invest.

An investor who starts at 25 with modest contributions will, in most historical scenarios, accumulate more wealth by retirement than an investor who starts at 35 with significantly larger contributions. Not because of superior strategy – because of the additional decade of compounding that can never be recovered.

This is the strongest possible argument for starting now, with whatever you have available, rather than waiting for better conditions or a larger amount.

“The best time to start investing was ten years ago. The second best time is today – with exactly what you have right now.”

A Practical Framework for Getting Started

You don’t need to resolve every question before taking the first step. You need a clear sequence.

1. Establish your financial foundation first. Before investing, ensure you have a basic emergency fund – three to six months of essential expenses in a liquid account. Investing money you may need in the short term creates pressure to sell at the wrong moment.

2. Open a brokerage account. Choose a platform that offers commission-free investing, access to low-cost index funds or ETFs, and automatic recurring investment options. The platform matters less than the act of opening it.

3. Start with a simple, diversified fund. A total market index fund or S&P 500 ETF provides immediate exposure to hundreds of companies. One fund, fully diversified, is a stronger starting point than five funds chosen without a clear framework.

4. Automate your contributions. Set up a recurring investment on the day after your paycheck arrives. Automation removes the decision from the equation each month – and decisions not made can’t be made incorrectly.

5. Add complexity only when simplicity has been mastered. Individual stocks, sector funds, alternative assets – these become relevant only after the foundational habit of consistent, diversified investing is established and stable.

Investing Is a Direction, Not a Destination

The goal of this guide isn’t to prepare you for every scenario you’ll encounter as an investor. That preparation happens through experience – through the market cycles you navigate, the decisions you get right and wrong, the lessons that only feel real when real money is involved.

The goal is to give you a clear enough starting point that you begin – and a simple enough framework that you continue.

Because in investing, continuity is the advantage. Not the best fund selection or the most sophisticated strategy. The willingness to stay invested, consistently, through the conditions that cause most people to stop.

“Investing success isn’t about making perfect decisions. It’s about making consistent decisions long enough for them to compound into something significant.”

That process starts with one account, one fund, one recurring contribution.

Everything else builds from there.

Tools to Help You Begin

| Tool | What It’s Good For | Link |

|---|---|---|

| Fidelity / Charles Schwab / Vanguard | Commission-free brokerage accounts with $0 minimums | Visit directly at fidelity.com, schwab.com, or vanguard.com |

| NerdWallet Investment Calculator (free) | Project how much your monthly contributions grow over time | nerdwallet.com/calculator/investment-calculator |

| Portfolio Visualizer (free) | Backtest simple 3-fund portfolio allocations historically | portfoliovisualizer.com |

| ETFdb.com (free) | Compare ETFs by expense ratio, holdings, and category | etfdb.com |

This article is for informational and educational purposes only and does not constitute financial advice. No affiliate relationships are currently in place for any platforms or tools mentioned in this post. Always consult a qualified financial professional before making investment decisions.

investing for beginners, how to start investing, beginner investing guide, stock market basics, etf investing, passive investing, long term investing, build wealth, personal finance, investment strategy, financial independence

Pingback: Stocks vs ETFs for Beginners: Which Investment Is Better for You?Stocks vs ETFs for Beginners: Which Investment Is Better for You? -

Pingback: How to Start Investing With $1,000: A Simple Beginner’s GuideHow to Start Investing With $1,000: A Simple Beginner’s Guide -

Pingback: How to Build a Simple Budget That Actually Works in 2026How to Build a Simple Budget That Actually Works in 2026 -

Pingback: The 5 Pillars of Smart Investing Every Beginner Should UnderstandThe 5 Pillars of Smart Investing Every Beginner Should Understand -

Pingback: Why an Emergency Fund is Your Ultimate Financial Safety Net -

Pingback: The Magic of Compounding: Why Time Is Your Greatest Investment AssetThe Magic of Compounding: Why Time is Your Greatest Investment Asset -

Pingback: Data-Driven Investment Insights: Precision Strategies for Modern Asset GrowthData-Driven Investment Insights: Precision Strategies for Modern Asset Growth -

Pingback: 3 Essential Principles for Navigating Volatile Markets in 20263 Essential Principles for Navigating Volatile Markets in 2026 -

Pingback: 2026 Global Market Trends: How to Navigate Volatility with Strategic Asset Allocation2026 Global Market Trends: How to Navigate Volatility with Strategic Asset Allocation -

Pingback: 24/7 Financial Navigation & Global Market Monitoring24/7 Financial Navigation & Global Market Monitoring -

Pingback: Passive Income From ETFs: How to Build Monthly Cash Flow With Minimal EffortPassive Income From ETFs: Build Cash Flow Without Managing Individual Stocks -

Pingback: How to Build Your First Investment Portfolio: A Beginner’s Step-by-Step GuideHow to Build Your First Investment Portfolio -

Pingback: Psychological Spending Triggers That Make You Spend Without Realizing ItPsychological Spending Triggers That Make You Spend Without Realizing It -

Pingback: The Simple 3 ETF Portfolio Strategy Most Beginners Should Start WithThe Simple 3 ETF Portfolio Strategy Most Beginners Should Start With -

Pingback: Which Is Better for Beginners ETFs or Stocks -

Pingback: What Is a Credit Score? Everything Beginners Need to KnowWhat Is a Credit Score? Everything Beginners Need to Know -

Pingback: How Your Credit Score Affects Interest RatesHow Your Credit Score Affects Interest Rates (And Why It Matters More Than You Think) -

Pingback: Investing for Beginners in Their 20s: The Complete 2026 PlaybookInvesting for Beginners in Their 20s: The Complete 2026 Playbook -

Pingback: Dollar-Cost Averaging vs Lump Sum Investing: Which Strategy Wins? -

Pingback: Why Beginners Lose Money Investing (And How to Stop It From Happening to You)Why Beginners Lose Money Investing (And How to Stop It From Happening to You) -

Pingback: How to Save $1,000 in 30 Days: A Realistic Step-by-Step PlanHow to Save $1,000 in 30 Days: A Realistic Step-by-Step Plan -