Most people know their credit score matters.

They just don’t know why – or how it actually works.

They know it’s a number. They know a higher number is better. And they know that when something important is on the line – an apartment, a car loan, a mortgage – that number suddenly becomes very relevant very fast.

But here’s the thing. A credit score isn’t some mysterious judgment handed down by an algorithm you can’t influence. It’s a calculation. A specific formula, built from specific inputs, producing a specific result.

And once you understand the inputs, you can start working with the formula instead of against it.

This guide explains everything from the beginning.

“A credit score is just math. And the good news about math is that it can always be improved.”

Where Credit Scores Come From

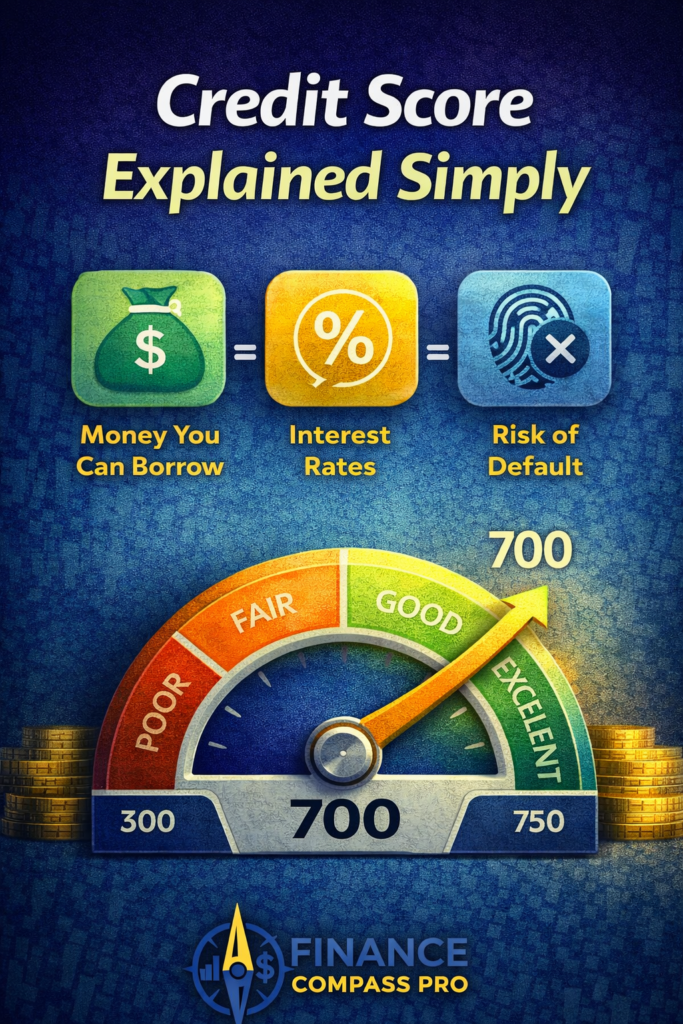

A credit score is a three-digit number – typically ranging from 300 to 850 – that represents how reliably you’ve managed borrowed money over time.

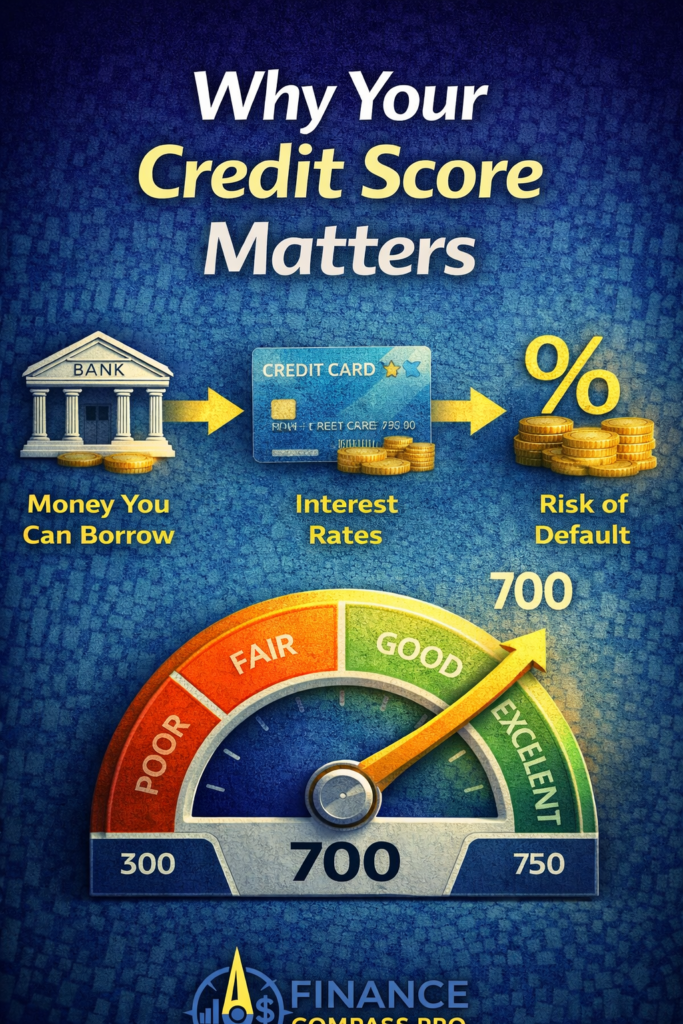

Lenders use it to make a simple decision: is this person likely to pay back what they borrow? The higher the score, the more confident a lender is in saying yes – and the better the terms they’re willing to offer you as a result.

The most widely used scoring model is the FICO score, developed by the Fair Isaac Corporation. You also have VantageScore, which was created jointly by the three major credit bureaus. Both use similar data and produce scores on the same scale, though the exact calculations differ slightly.

When a lender checks your credit, they’re almost always pulling one of these two models – most commonly FICO.

The Five Factors That Build Your Score

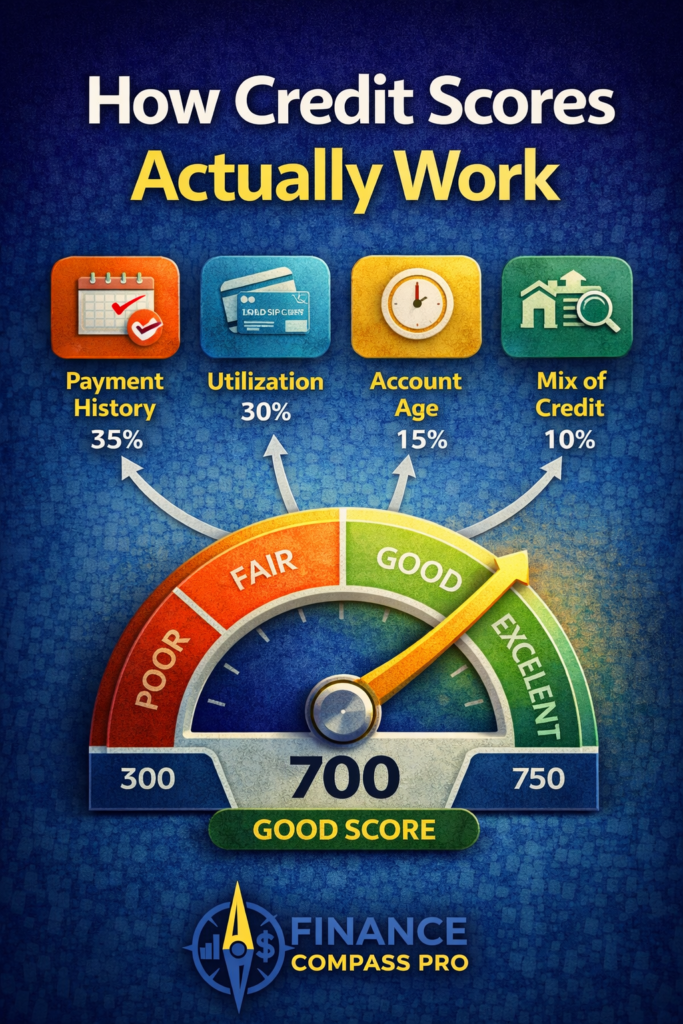

Your credit score isn’t generated randomly. It comes from five specific factors, each weighted according to how predictive it is of future repayment behavior.

Payment history carries the most weight at 35 percent of your total score. This factor asks one question: do you pay your bills on time? Every on-time payment builds it. Every missed or late payment damages it. There is no single factor more important to get right.

Credit utilization accounts for 30 percent. This measures how much of your available credit you’re currently using. If your total credit limit across all cards is $10,000 and your current balances total $4,000, your utilization is 40 percent. Most experts recommend keeping this below 30 percent. The best scorers stay below 10 percent.

Length of credit history makes up 15 percent of your score. This rewards accounts that have been open and active for a long time. The longer your average account age, the better. This is one reason closing old credit cards – even ones you rarely use – can quietly hurt your score.

Credit mix accounts for 10 percent. This factor reflects whether you have experience managing different types of credit: credit cards, installment loans, auto loans, mortgages. A mix signals to lenders that you can handle multiple types of financial obligations responsibly.

New credit inquiries make up the final 10 percent. Every time you formally apply for new credit, a hard inquiry is added to your report. One or two hard inquiries have a minor, temporary impact. Multiple applications in a short period can compound into something more significant.

| Factor | Weight | What It Measures |

|---|---|---|

| Payment History | 35% | On-time vs. missed/late payments |

| Credit Utilization | 30% | Balance used vs. total credit limit available |

| Length of Credit History | 15% | Average age of all open accounts |

| Credit Mix | 10% | Variety of credit types (cards, loans, mortgage) |

| New Credit Inquiries | 10% | Hard inquiries from recent credit applications |

Understanding these five factors doesn’t just explain the number. It shows you exactly where to focus your energy if you want to change it.

What the Numbers Actually Mean

Credit scores are grouped into ranges, and each range carries a different meaning to the lenders looking at them.

A score below 580 is generally considered poor. At this level, approval for most credit products is difficult, and the rates offered when approval does happen tend to be significantly higher than average.

Scores from 580 to 669 fall into the fair range. Approval is more likely, but the terms won’t be favorable. You’ll pay more in interest than someone with a stronger score.

From 670 to 739 is considered good – the range where most standard financial products become accessible at reasonable rates. This is where things start to open up meaningfully.

Scores from 740 to 799 are very good. Lenders compete for borrowers in this range. Interest rates improve noticeably and approval odds are high across most products.

800 and above is exceptional. At this level, you’re likely to qualify for the best rates available and experience essentially no friction in the lending process.

The practical difference between a 620 and a 750 on a 30-year mortgage isn’t just a number on a page. It can translate to tens of thousands of dollars in total interest paid over the life of the loan.

| Score Range | Rating | What It Means in Practice |

|---|---|---|

| 800 – 850 | Exceptional | Best rates available, essentially no approval friction |

| 740 – 799 | Very Good | Lenders compete for you; strong rates across all products |

| 670 – 739 | Good | Standard products accessible at reasonable rates |

| 580 – 669 | Fair | Approval possible but rates are unfavorable |

| 300 – 579 | Poor | Most approvals denied; high rates when approved |

Where Your Credit Data Actually Lives

Your credit score is generated from data in your credit report – and those reports are maintained by three separate companies: Equifax, Experian, and TransUnion.

Each bureau collects data independently. That means the information on your Equifax report may differ slightly from what’s on your TransUnion report, which is why your score can vary depending on which bureau a lender pulls.

In the United States, you’re entitled to one free report from each bureau every 12 months through AnnualCreditReport.com. That’s three reports per year, and it costs nothing.

Pulling your own credit report does not affect your score. That’s a soft inquiry. Only applications for new credit – initiated by lenders in response to an application you submitted – generate hard inquiries that affect your score.

This is worth knowing because many people avoid checking their own credit out of fear it will hurt them. It won’t. Checking your report is the first step toward understanding and improving it.

The Difference Between a Credit Score and a Credit Report

These two terms are related but not the same thing – and the distinction matters.

Your credit report is the raw data. It’s a detailed record of every credit account you’ve ever opened, every payment you’ve made or missed, every hard inquiry on your file, and any public records like bankruptcies or collections. It’s the source material.

Your credit score is what gets calculated from that source material. It’s the number that results from running your credit report data through a scoring formula.

If your score is low, the reason is somewhere in your report. That’s where you look first – not just at the number, but at the underlying data generating it. Errors in your report are more common than most people expect, and a single incorrect late payment or fraudulent account can suppress your score by 50 points or more.

How Credit Scores Affect Your Financial Life

The reach of your credit score extends further than most people realize until they encounter it somewhere unexpected.

The most obvious applications are lending. Mortgages, auto loans, personal loans, and credit cards all involve a credit check. Your score determines whether you’re approved and at what rate.

But it goes beyond borrowing. Many landlords pull credit before approving a rental application. Some employers check credit as part of background screening, particularly for financial roles. Insurance companies in many states use credit-based insurance scores to set premiums.

This is why building and protecting your credit score matters even when you’re not actively borrowing. The score you have when you need it is the one you built before you needed it.

How Your Credit Score Affects Interest Rates (And Why It Matters More Than You Think)

How Long Negative Items Stay on Your Report

One of the most common sources of anxiety around credit is the question of how long a mistake follows you.

The answer depends on the type of item. Late payments stay on your report for seven years from the date of the missed payment. Collections accounts also remain for seven years. A Chapter 7 bankruptcy stays for ten years. Hard inquiries from credit applications fall off after two years.

These timelines feel long. But there’s important nuance here: the impact of a negative item diminishes significantly over time. A late payment from five years ago affects your score far less than a late payment from five months ago. Lenders weight recent history more heavily than older history.

The practical implication is that no matter where your credit stands right now, consistent positive behavior going forward starts improving your score relatively quickly – even before negative items fall off entirely.

Credit Scores and Investing: The Connection Most People Miss

There’s a relationship between your credit score and your ability to build wealth that doesn’t get discussed enough.

A strong credit score reduces the cost of borrowing. A lower interest rate on a mortgage frees up cash flow that can go toward investing instead of interest payments. A better rate on a car loan means more of your income is available each month to put toward your financial goals.

In that sense, your credit score isn’t just a lending tool – it’s a lever on how efficiently you can build wealth over time.

If you’re working on your credit foundation while simultaneously learning how to invest, these two things aren’t separate tracks. They’re part of the same financial system.

Investing for Beginners: The Complete Guide to Building Wealth in 2026

What Is Dollar-Cost Averaging and Why Smart Investors Use It

How to Start Investing with $1,000: A Simple Beginner’s Guide

What Doesn’t Affect Your Credit Score

Just as important as knowing what goes into your score is knowing what doesn’t.

Your income has no effect on your credit score. A high earner with a history of missed payments will have a lower score than someone earning much less who pays every bill on time. Income matters to lenders for different reasons – it affects debt-to-income ratio – but it doesn’t factor into the score calculation itself.

Your age, gender, marital status, race, and nationality are legally prohibited from being used in credit scoring under the Equal Credit Opportunity Act.

Checking your own credit – through a free monitoring service or AnnualCreditReport.com – does not affect your score. Neither does being denied credit. And having savings or investments in a bank or brokerage account has no effect on your credit score whatsoever.

Building Credit When You’re Starting From Zero

Having no credit history is a different problem from having bad credit – but it presents similar obstacles.

Lenders are reluctant to extend credit to someone with no track record. And you can’t build a track record without someone extending you credit first. It’s a genuine catch-22.

The most practical solutions for building credit from scratch involve tools specifically designed for the purpose. A secured credit card – where you deposit funds that become your credit limit – lets you use credit normally while the issuer takes on minimal risk. A credit-builder loan, offered by many credit unions and community banks, works in reverse: you make payments into a savings account that you receive at the end of the term, while the payment history gets reported to the bureaus.

Both approaches are slow. That’s the point. Credit is built over time, not overnight. But the system rewards consistency – and a few months of responsible use on a starter product can establish enough of a foundation to start accessing more mainstream credit products.

How to Improve Your Credit Score Fast in 30 Days

The Bottom Line

A credit score is not a permanent verdict on your financial character.

It’s a snapshot of how you’ve managed credit up to this point, calculated from a defined set of inputs that you have real influence over. Every on-time payment improves it. Every reduction in utilization improves it. Every year of maintained accounts and avoided unnecessary hard inquiries improves it.

The people with the highest scores didn’t get there by accident. They understood what the formula rewards – and they built their habits around it.

Understanding your credit score is the first step. What you do with that understanding is what changes the number.

Ready to take the next step?

How to Improve Your Credit Score Fast in 30 Days

Investing for Beginners: The Complete Guide to Building Wealth in 2026

What Is Diversification in Investing?

This article is for informational and educational purposes only and does not constitute financial advice. No affiliate relationships are currently in place for any tools or services mentioned in this post. Always consult a qualified financial professional before making financial decisions.

what is a credit score, credit score explained, how credit scores work, credit score for beginners, FICO score

Pingback: 3 Reasons Why Your Credit Score Matters More Than You Think -

Pingback: Smart Credit & Wealth Planning: Strategies for Long-term Prosperity -

Pingback: Psychological Spending Triggers That Make You Spend Without Realizing ItPsychological Spending Triggers That Make You Spend Without Realizing It -

Pingback: How to Improve Your Credit Score Fast in 30 DaysHow to Improve Your Credit Score fast In 30 days -

Pingback: How Your Credit Score Affects Your Financial Future -

Pingback: How Your Credit Score Affects Interest RatesHow Your Credit Score Affects Interest Rates (And Why It Matters More Than You Think) -